Global Logistics Update

U.S. Announces Trade Deal with China; TPEB Sees Slight Ease in Demand

North America vessel dwell times and other updates from the global supply chain | May 17, 2023

Global Logistics Update: June 12, 2025

Trends to Watch

Talking Tariffs

This week, Flexport released a new, complimentary Customs Guide that dives into six critical importer strategies. Learn how to mitigate tariff impacts, reduce compliance risks, and recover costs where possible. Additionally, calculate and analyze tariff impacts in real time with Flexport’s recently launched Tariff Simulator.

- President Trump Announces Trade Deal with China: On June 11, President Trump announced on Truth Social that the U.S. and China had struck a trade deal, pending final approval from both himself and President Xi. The announcement came after U.S. and Chinese trade representatives met in London for two days of trade talks. The agreement includes:

- A 55% total tariff rate on Chinese goods imported into the U.S. (comprised of a 10% baseline IEEPA reciprocal tariff, a 20% IEEPA “fentanyl” tariff, and a 25% tariff that includes levies imposed during the president’s first term)

- A 10% total tariff rate on U.S. goods imported into China

- A streamlined process for importing Chinese rare earth shipments into the U.S.

- Resumed access to U.S. colleges and universities for Chinese nationals

- U.S. Court of Appeals Keeps IEEPA Tariffs in Place as Appeals Proceed: On June 10, the U.S. Court of Appeals for the Federal Circuit issued a longer-term stay that will keep President Trump’s IEEPA tariffs in place as litigation proceeds.

- The longer-term stay follows a temporary stay issued by the appeals court on May 29, which came less than a day after the Court of International Trade (CIT) initially invalidated four of President Trump’s executive orders on tariffs imposed under IEEPA.

- Both parties will prepare for oral arguments, which will be heard by the appeals court on July 31, 2025.

- The Latest on Reciprocal Tariffs:

- On June 11, Treasury Secretary Scott Bessent indicated it is “highly likely” that the July 9 end date for the 90-day country-specific reciprocal tariff pause will be extended for “top U.S. trading partners” involved in “good faith” trade negotiations. Additionally, President Trump’s proposed 50% tariff on the EU—currently postponed until July 9—is likely to be pushed back further.

- Chinese-origin goods with a time of entry on or after May 14, 2025, are subject to a 10% reciprocal tariff until August 11, 2025. Afterwards, in the absence of a deal, the reciprocal tariff rate will revert back to 34%. However, if President Trump and President Xi approve and implement the trade deal announced on June 11, China will be subject to a 10% reciprocal tariff rate (total effective tariff rate of 55%).

- We expect the reciprocal tariff rate on the U.K. to remain at 10% due to the previously announced trade deal.

- Goods from other countries of origin are subject to a 10% reciprocal tariff until July 9, 2025. If the U.S. and those countries of origin do not reach deals by July 9, country-specific duty rates are set to kick in again.

- Any HTS in Annex II is exempt from reciprocal tariffs, regardless of the country of origin. As of April 16, 2025, semiconductor products are also excluded from reciprocal tariffs.

Get the latest updates and guidance on U.S. tariffs and trade on our live blog.

Ocean

TRANS-PACIFIC EASTBOUND (TPEB)

- Demand and Market Dynamics: Demand for TPEB shipping remains strong, driven by factors like potential tariff changes (e.g., the expiration of both the temporary U.S.-China trade agreement in August, and the 90-day country-specific reciprocal tariff pause on July 9), along with the upcoming annual peak season. However, new booking intakes have slowed since early June, indicating some ease in demand.

- Capacity Outlook: More capacity is being restored and is opening up across various gateways.

- Pacific Southwest (PSW) gateways are seeing increased capacity availability, with more extra loaders being deployed.

- Pacific Northwest (PNW) gateways are experiencing some softening and open space.

- The East Coast and Gulf regions remain firmer due to less significant capacity injection compared to the West Coast. One extra loader has been deployed into the East Coast, and another East Coast service is scheduled to resume starting Week 28.

- This week (Week 24), offered capacity on the TPEB is 5% below standard levels (+5% WoW), and is expected to exceed standard levels by 4% next week (Week 25).

- Overall capacity for the remainder of June is expected to range between 74% and 83%. July capacity is forecasted to increase further, reaching around 90%.

- Blank Sailings: Sailing cancellations continue to fall. This week, we saw a cancellation rate of 9% (vs. 34% in early May). In the second half of June, blank sailings are projected to decline further, with an expected cancellation rate of just 5% in Week 26—the fewest blank sailings since late March.

- Equipment:

- Equipment availability generally remains sufficient across the TPEB lane.

- Container shortages are not an immediate concern, though the situation remains fluid.

- Freight Rates:

- West Coast rates are quickly mitigating and still downtrending for the remainder of June.

- East Coast and Gulf rates are holding firmer due to less capacity injection.

- The General Rate Increase (GRI) for June 15 has been fully withdrawn for West Coast destinations. For the East Coast and Gulf, a GRI remains in effect, pending further confirmation from carriers.

- The Peak Season Surcharge (PSS) for June 15 has been extended until the end of June, per confirmation from a few carriers.

FAR EAST WESTBOUND (FEWB)

- Capacity and Demand:

- Carrier vessel utilization remains extremely high, with most near-term sailings fully booked.

- Carriers recommend that bookings be made at least three weeks in advance to secure both space and equipment.

- Downsized vessels and upcoming mid-June blank sailings are contributing to the current tightness in capacity. Additionally, vessel delays are further impacting on-time departures.

- Freight Rates:

- The Shanghai Containerized Freight Index (SCFI) for the FEWB trade has risen by 44% over the past four weeks. Despite the implementation of the early June GRI, demand has continued to climb, prompting carriers to maintain elevated rates and push for further increases. Carriers have already announced a GRI for the second half of June, with the market now targeting rates above 3,000 USD/FEU.

- Ongoing vessel delays, blank sailings, and equipment shortages have resulted in cargo rollovers, supporting the upward momentum in the market.

- Additionally, more customers are inquiring about July export plans, indicating persistent market anxiety and a surge in bookings. In the short term, rates are expected to remain on an upward trend.

- Shippers are advised to finalize export plans as early as possible. Delayed bookings can result in cargo delays and increased costs.

- Shippers are also advised to arrange for early container pick-up, and closely monitor shipments at every stage to ensure smooth operations and avoid unnecessary loss of space.

TRANS-ATLANTIC WESTBOUND (TAWB)

- Capacity and Demand: Congestion remains at European ports.

- Northern European ports still face delays and long wait times.

- In the Mediterranean, congestion has not improved. Wait times remain unchanged at ports in Greece, Spain, and Northern Italy.

- Equipment:

- European ports are not currently facing any major equipment shortages. There are slight deficits in Scan Baltic ports (in Sweden, Lithuania, Estonia, Finland, and Norway), the Port of Mersin in Southern Turkey, and Lisbon and Leixoes in Portugal.

- Equipment shortages persist in parts of Central Europe, particularly in Austria, Slovakia, Switzerland, Hungary, and Southern/Eastern Germany. Carrier haulage is recommended for these origins.

- Freight Rates:

- North Europe: Carriers are postponing their PSSs until July.

- West Mediterranean: One carrier is attempting to implement a PSS in the last week of June, while the rest have postponed it until July.

- East Mediterranean: Carriers have further postponed their PSSs until July, while other carriers have postponed it until further notice.

INDIAN SUBCONTINENT TO NORTH AMERICA

- Capacity and Demand:

- Capacity to the U.S. West Coast is limited due to direct services, which also call on Chinese and Vietnamese ports of loading, along with increases in bookings from those regions (China and Vietnam).

- Capacity to the U.S. East Coast is greater due to numerous direct services in the market, which are Indian-subcontinent-specific ports of loading. Carriers are reporting that they are running ships fully utilized on such services. There are multiple blank sailings on routes from Northwest India to the U.S. East Coast for the month of June, reducing capacity.

- Freight Rates:

- For Indian subcontinent cargo moving to the U.S. West Coast, GRIs and PSSs have been announced for the second half of June in light of pressure on capacity stemming from booking increases from China and Vietnam to the U.S.

- For cargo moving to the U.S. East Coast, GRIs and PSSs were implemented in the first half of June. It is possible that these will soften, given that bookings have not ticked up in large quantities.

- Exports from Pakistan are seeing increases due to additional feeder services being launched in light of the India-Pakistan conflict.

Air

WEEK 22: MAY 26 - JUNE 1, 2025

- A Rebound in Tonnages, Despite Volatility: Global air cargo volumes rose +4% month-on-month (MoM) and +4% year-on-year (YoY) in May, rebounding from a -7% MoM drop in April. Recovery was driven by the U.S.-China tariff de-escalation in mid-May, which restored demand on the Trans-Pacific lane after early-month weakness.

- Regional Volume Growth: May YoY volume increases were led by the Asia-Pacific (+7%), Europe (+4%), and Central and South America (+3%). North America (+1%) and Africa (+2%) saw smaller gains, while the Middle East and South Asia (MESA) remained flat YoY.

- Rates Under Pressure: Average global air cargo rates fell -4% MoM and -3% YoY in May. The steepest YoY rate drop came from MESA (-14%), while Africa was the only region without a recorded decline.

- Week 22 Holiday Dip and Rate Movements: In Week 22 (May 26–June 1), global tonnages fell -8% WoW, led by North America (-13%) and Europe (-11%) due to holidays. However, average spot rates from the Asia-Pacific rose +4% WoW to 3.68 USD/kg, with Hong Kong–U.S. lanes up +9% WoW to 4.76 USD/kg. Despite weekly gains, China/HK–U.S. volumes remained -8% YoY.

(Source: WorldACD)

Please reach out to your account representative for details on any impacts to your shipments.

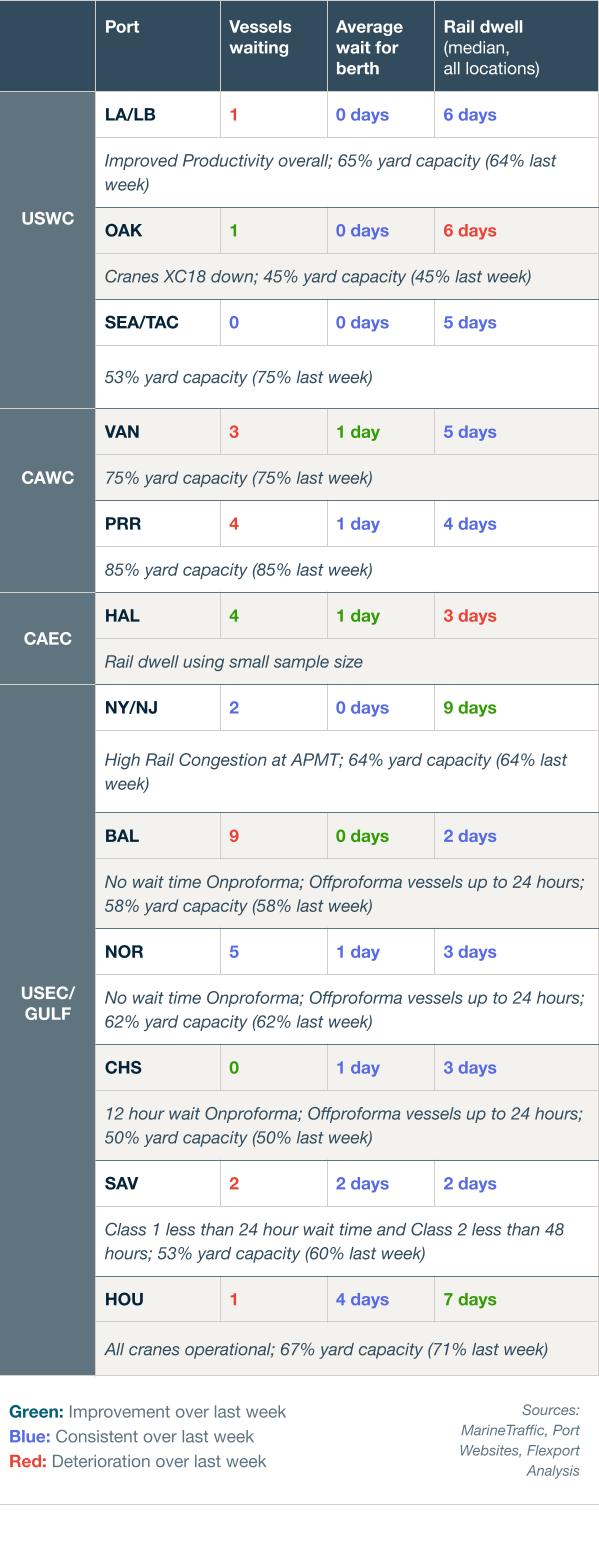

North America Vessel Dwell Times

Upcoming Webinars

Tariff Trends 2025: Expert Insights on the New U.S. Customs Landscape

Thursday, June 26 @ 8:00 am PT / 11:00 am ET / 16:00 BST / 17:00 CEST

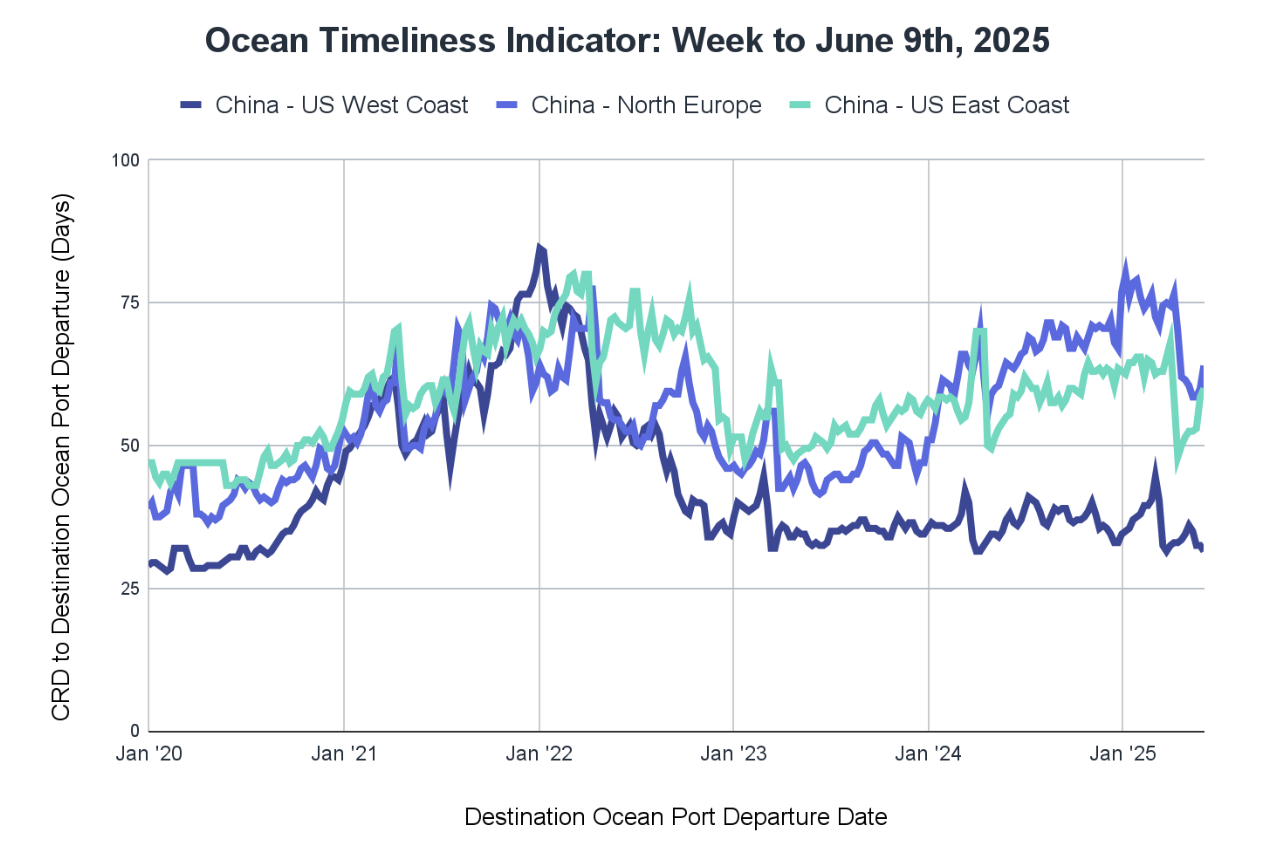

Ocean Timeliness Indicator

This week, the Flexport OTI for China to the U.S. West Coast fell slightly, China to North Europe jumped, and China to the U.S. East Coast increased slightly.

Week to June 9, 2025

The Ocean Timeliness Indicator (OTI) for China to the U.S. West Coast dropped by a point, from 32.5 to 31.5 days. Meanwhile, China to North Europe jumped, rising from 60 to 64 days. China to the U.S. East Coast showed a small uptick, increasing from 58.5 to 60 days.

About the Author

Related content

更多

![WarehouseGettyImages-535667233]()

Global Logistics Update

U.S. and Taiwan Finalize Trade Deal; FEWB Spot Rates Soften Amid Lunar New Year Lull

![Ocean Port GettyImages-1083936322 (1)]()

Global Logistics Update

EU to Vote on Modified U.S. Trade Deal; Ex-Asia Demand Tapers Off Ahead of Lunar New Year

![Air GettyImages-1343405900]()

Global Logistics Update

U.S. to Cut Tariffs on India; TPEB and FEWB Carriers Plan Upcoming Blank Sailings