Global Logistics Update

Federal Court Invalidates IEEPA Tariff Executive Orders; TPEB Volumes Surge Amid Demand Spike

North America vessel dwell times and other updates from the global supply chain | May 17, 2023

Global Logistics Update: May 29, 2025

Trends to Watch

Talking Tariffs

We launched the Flexport Tariff Simulator. Estimate and forecast tariffs and landed costs for each shipment, all based on real-time data and the latest rates and regulations.

- Court of International Trade (CIT) Invalidates Four Executive Orders: Yesterday (May 28), the U.S. Court of International Trade invalidated four of President Trump’s executive orders on tariffs imposed under the International Emergency Economic Powers Act (IEEPA): the 25% IEEPA tariffs on Canada and Mexico, the 20% IEEPA tariff on China, and country-specific IEEPA reciprocal tariffs (ranging from 10-67%, and formerly 125% on China).

- According to the court, President Trump’s invocation of IEEPA to enact these tariff orders “exceeds any authority granted to the president … to regulate importation by means of tariffs.”

- The court has ordered Customs and Border Protection (CBP) to stop collecting duties from these tariff orders within 10 days.

- Section 301 and Section 232 duties remain in place, and are not impacted by yesterday’s ruling.

- The Trump administration has appealed the decision, asking the U.S. Court of Appeals for the Federal Circuit to stay the order. If that stay is granted, the invalidation of the IEEPA duties will not be implemented, and the current tariffs would remain in effect.

- What happens next? The U.S. Court of Appeals will review the CIT decision and weigh in. Afterwards, the losing side will likely appeal to the Supreme Court.

- We could be months away from a final decision on these tariffs, but given the national importance of this case, resolution may come sooner.

- Get the full update on our live blog for more details on yesterday’s ruling, along with other tools the Trump administration could leverage to impose tariffs.

- President Trump Delays 50% Tariff on EU: On May 25, 2025, President Trump announced that he would delay implementing a 50% tariff on the EU until July 9, 2025. Just two days prior to the announcement, President Trump had suggested that the 50% tariff take effect on June 1, 2025 instead. In light of the extension until July 9, the U.S. and the EU will proceed with negotiations, which are set to “begin rapidly.”

- The End of Certain Section 301 Exclusions: Some exclusions from China Section 301 tariffs are set to expire on May 31, 2025.

- 9903.88.69: Exclusions from duties ranging from 7.5-25%. These are extensions of previously granted exclusions on a wide range of goods, including compressors, pool cleaning robots, tiles, pumps, car seats, and more.

- 9903.88.70: Specific carveouts from Section 301 duties for chip-making equipment and machines. These exclusions were originally enacted via the CHIPS Act, introduced under the Biden administration in an effort to promote domestic production.

- President Trump’s Proposed “Big Beautiful Bill”: The One Big Beautiful Bill, President Trump’s proposed budget reconciliation and tax cut bill, would ban the de minimis exemption altogether by July 1, 2027, through the enactment of the main portion of the proposed FIGHTING for America Act.

- If enacted, the One Big Beautiful Bill would also impose various penalties on those who import goods under the de minimis exemption in violation of any other U.S. law prior to July 1, 2027: 5,000 USD for the first violation, and up to 10,000 USD for each subsequent violation.

- The One Big Beautiful Bill narrowly passed the House of Representatives on May 22, 2025, and will move on to the Senate sometime in June.

- The de minimis exemption expired for goods from China and Hong Kong on May 2, 2025. Per President Trump’s Liberation Day executive order, de minimis will be eliminated for all U.S. trade partners once “adequate systems are in place to fully and expeditiously process and collect duty revenue.”

- The Latest on Reciprocal Tariffs:

- Chinese-origin goods with a time of entry on or after May 14, 2025, are subject to a 10% reciprocal tariff until August 11, 2025. On August 12, the reciprocal tariff rate will increase to 34%.

- Goods originating from Great Britain are subject to an indefinite 10% reciprocal tariff.

- Goods from other countries of origin are subject to a 10% reciprocal tariff until July 9, 2025. If the U.S. and those countries of origin do not reach deals by July 9, country-specific duty rates are set to kick in again.

- Any HTS in Annex II is exempt from reciprocal tariffs, regardless of the country of origin. As of April 16, 2025, semiconductor products are also excluded from reciprocal tariffs.

Ocean

TRANS-PACIFIC EASTBOUND (TPEB)

- Increased Demand and Cargo Rush:

- Demand is currently strong, with volumes surging into June and continuing to increase.

- A further rush of cargo from Southeast Asia to the U.S. West Coast is anticipated toward the end of June as the 90-day tariff pause ends on July 9 (and the reduced tariff on Chinese-origin goods ends on August 11), prompting shippers to move cargo before potential tariff increases.

- With the increased demand, vessel capacity is being booked up. Shippers are advised to book four weeks in advance and use premium options if urgency is a priority. Reach out to your Flexport representative for more information on premium options.

- Increased Capacity and Service Resumptions:

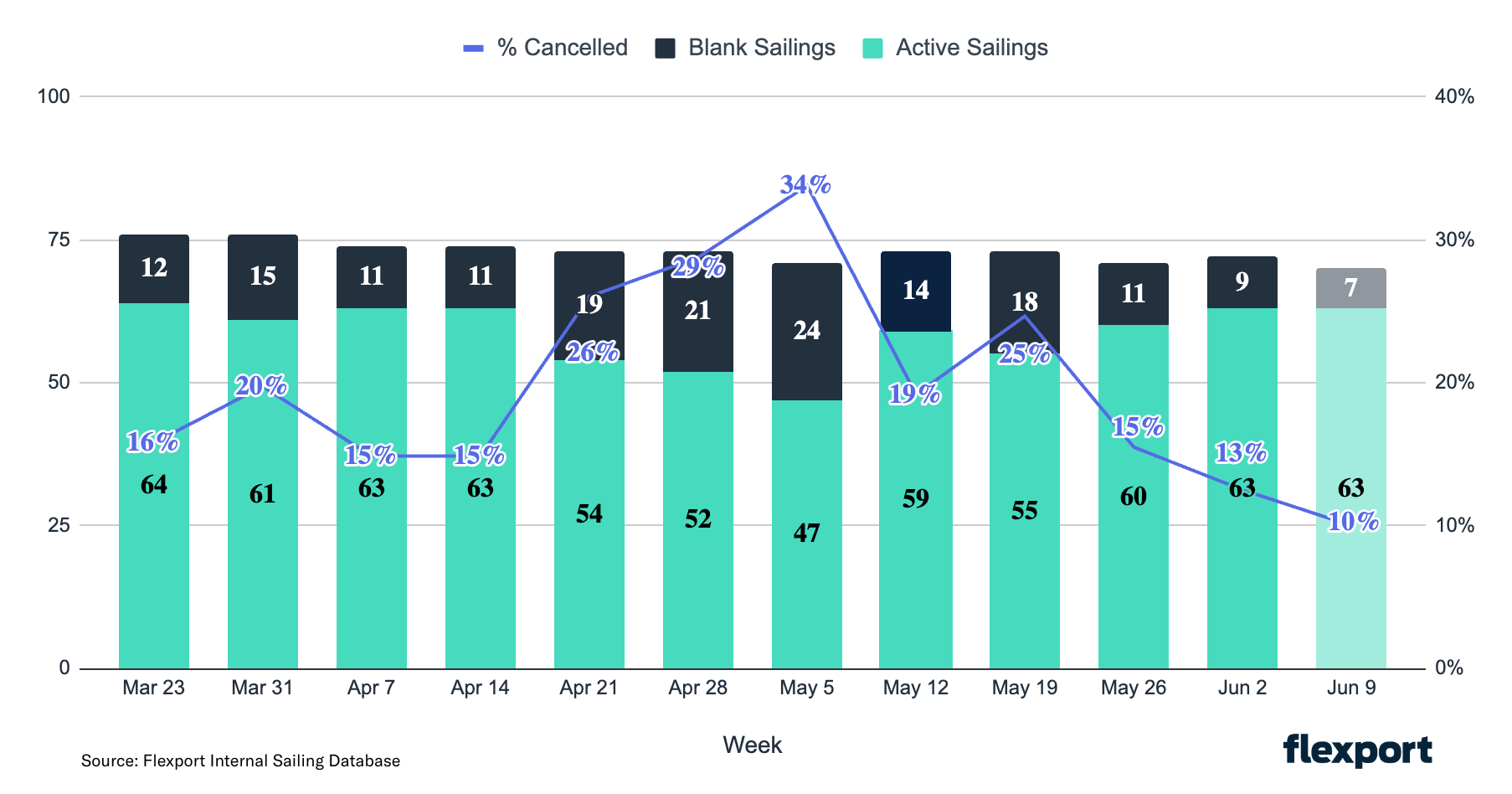

- Capacity Restoration: Carriers are actively working to restore capacity, with expectations of full capacity being back by the end of June. This week (Week 22), capacity is 9% below standard below standard levels; by Week 24, capacity is forecasted to improve further, at just 4% below standard levels.

- Current Utilization: As of June, overall capacity is estimated at between 80% and 86%.

- Blank Sailings: This week, we saw a cancellation rate of 15% (-10% WoW). Blank sailings are forecasted to decrease further in the coming weeks, with a projected 10% cancellation rate the week of June 9—the fewest blank sailings since late March.

- Extra Loaders and Resumed Services: Multiple carriers have deployed extra loader vessels and resumed previously suspended services to meet increased demand.

- A total of seven (out of ten) suspended TPEB service loops are now scheduled to resume, some beginning this week. See our updated blog for more details.

- Equipment: Equipment availability generally remains sufficient, and container shortages are not an immediate concern.

- Freight Rates:

- GRI and PSS Implementation: The General Rate Increases (GRIs) and Peak Season Surcharges (PSSs) for June 1 have been finalized, and are expected to be fully and firmly implemented.

- Factors Driving Increases: This firm implementation is attributed to surging demand, coupled with capacity that has not yet fully recovered on the TPEB market, affecting both floating (spot) and fixed rates.

FAR EAST WESTBOUND (FEWB)

- Capacity and Demand:

- Space is quickly tightening, with the end of May bringing a major squeeze on available capacity. Carriers are taking more space control measures on allocations, leading to more cargo rolling and space issues in the coming weeks. The market continues to increase with regard to both rates and volumes.

- Early June vessels are filling up fast, with carriers already warning of worsening equipment shortages next month. Shippers are advised to move quickly, prioritize efficient pickups, and book early to avoid delays.

- Destination port congestion is worsening, and European ports are seeing serious delays. Wait times are spiking across the board, with notable increases in berth wait times (vs. Week 13) at the following main ports of destination (PODs): Bremerhaven (+77%), Hamburg (+49%), and Antwerp (+37%). Rotterdam and Felixstowe are also exhibiting longer dwell times than usual.

- The June GRI announcement has triggered a noticeable spike in bookings, boosting overall market demand over the past two weeks.

- With ongoing vessel delays at key ports of loading (POLs) like Shanghai and Ningbo, we anticipate this cargo rush could extend for several more weeks—even with the upcoming GRI implementation in June, which is expected to drive ocean freight rates up by nearly 1.5x.

- Freight Rates:

- The June GRI might take full effect, with rates in the first week of June likely to remain high until congestion at POLs and equipment shortages show signs of improvement.

- As the market continues its upward trend, the balance between Named Account Contract (NAC) and Freight All Kinds (FAK) rates is gradually normalizing. However, given persistent space and equipment constraints, carriers may reassess clients' previous performance and adjust NAC allocation shares in the coming weeks.

TRANS-ATLANTIC WESTBOUND (TAWB)

- Capacity and Demand: Congestion persists at the ports of Antwerp, Rotterdam, Bremerhaven, and London Gateway in North Europe, and Piraeus, Genoa, and Valencia in the Mediterranean. This has resulted in ongoing delays and impacts to schedule reliability. In Antwerp in particular, delays have increased substantially due to recent strikes.

- Equipment: Equipment shortages persist in parts of Central Europe, particularly in Austria, Slovakia, Switzerland, Hungary, and Southern/Eastern Germany. Carrier haulage is recommended for these origins. Mersin and Aliaga in Turkey and Lisbon in Portugal continue to face equipment shortages, and carriers are continuing to carry out empty repositions to support demand.

- Freight Rates:

- North Europe: The majority of carriers have not implemented a PSS for June, except a few that have implemented PSSs on their FAK rates.

- West Mediterranean: Some carriers have announced PSSs that will be implemented beginning the second half of June.

- East Mediterranean: Some carriers have further postponed their PSSs until the second half of June, some until July, and others until further notice.

INDIAN SUBCONTINENT TO NORTH AMERICA

- Capacity and Demand:

- Capacity to the U.S. West Coast is constrained due to limited direct services, which also call on Chinese and Vietnamese ports of loading.

- Capacity to the U.S. East Coast is greater due to numerous direct services in the market, which are Indian-subcontinent-specific ports of loading.

- Demand remains stable, as carriers are reporting vessels running highly utilized.

- Freight Rates:

- For Indian subcontinent cargo moving to the U.S. West Coast, GRIs and PSSs are hitting the market in the first half of June in light of pressure on capacity stemming from booking increases from China and Vietnam to the U.S.

- Exports from Pakistan are seeing increases due to additional feeder services being launched in light of the India-Pakistan conflict.

Air

WEEK 20: MAY 12 - MAY 18, 2025

- Global Air Cargo Volumes Rebounded +6% WoW: The rebound was driven by a strong +11% increase from the Asia-Pacific. Key recoveries came from Japan (+60%) post-Golden Week, South Korea (+21%) post-Children’s Day, and China and Hong Kong (+8%), which together contributed around two-thirds of the global uplift.

- U.S.-China Traffic Surged +19% WoW: Following the May 12 interim tariff deal, U.S.-China traffic increased +19% WoW, reversing two weeks of declines after the May 2 de minimis expiration. Volumes are now near early April levels; spot rates on this lane have stabilized at ~4 USD/kg.

- China to Europe Volumes Rose +9% WoW: The +9% WoW increase has pushed total China-HK exports to Europe close to their highest 2025 levels. Rate trends diverged: China-Europe spot rates fell -5% WoW to 3.71 USD/kg, while HK-Europe rates rose +2% to 4.39 USD/kg—still well below peak season averages.

- Central and South America Volumes Dropped -23% (2Wo2W): After flower demand eased post-Mother’s Day (May 11), Central and South America volumes dropped -23% vs. the two weeks prior, with -4% WoW from Central and South America and -2% WoW from North America.

- Global Average Rates Rose +2% WoW: Despite Central and South America volume declines, global average rates rose +2% WoW to 2.33 USD/kg, but remain -4% YoY. Middle East and South Asia (MESA) spot rates plunged -23% YoY, the steepest regional decline.

(Source: WorldACD)

Please reach out to your account representative for details on any impacts to your shipments.

North America Vessel Dwell Times

Upcoming Webinars

Tariff Trends 2025: Expert Insights on the New U.S. Customs Landscape

Wednesday, June 4 @ 8:00am PT / 11:00 am ET / 16:00 BST / 17:00 CEST

European Freight Market Update Live

Tuesday, June 10 @ 15:00 BST / 16:00 CEST

North America Freight Market Update Live

Thursday, June 12 @ 9:00 am PT / 12:00 pm ET

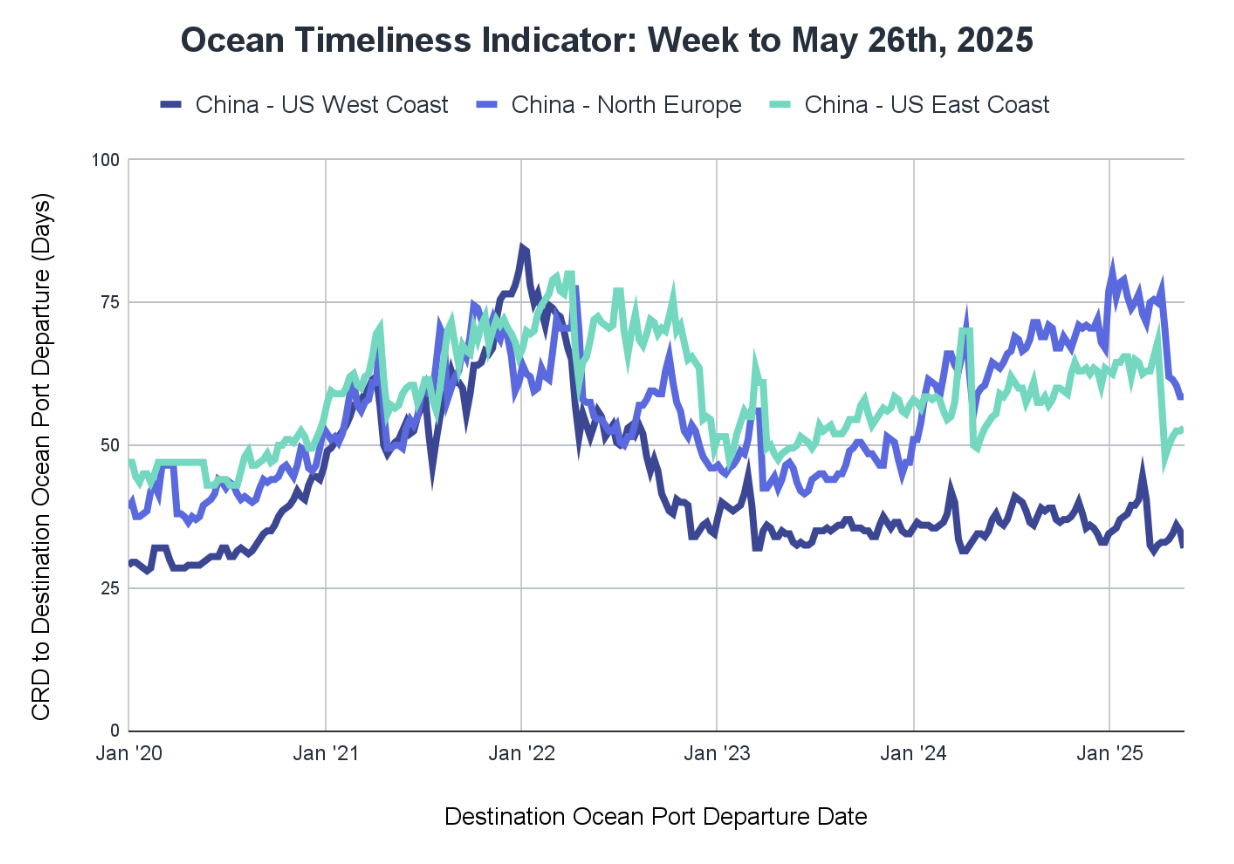

Ocean Timeliness Indicator

This week, the Flexport OTI for China to the U.S. West Coast declined, China to North Europe remained stable, and China to the U.S. East Coast increased.

Week to May 26, 2025

The Ocean Timeliness Indicator (OTI) for China to the U.S. West Coast decreased from 35 to 32 days, while China to North Europe plateaued at 58.5 days. Meanwhile, China to the U.S. East Coast increased from 52.5 to 53 days.

About the Author