Global Logistics Update

President Trump Suggests Possible New Tariffs; Demand for Ex-India Air Freight Skyrockets

North America vessel dwell times and other updates from the global supply chain | May 17, 2023

Global Logistics Update: August 28, 2025

Trends to Watch

Talking Tariffs

- President Trump Announces Potential Duties Targeting Digital Service Taxes: On August 25, President Trump indicated plans to impose “substantial additional tariffs” on nations that do not remove digital taxes and regulations, citing discriminatory practices targeting American technology companies. These nations would also face restrictions on U.S. chip exports, he added.

- The U.K., which reached a trade agreement with the U.S. in May, continues to impose digital service taxes.

- The EU, which also recently struck a trade deal with the U.S., does not directly impose digital service taxes. Instead, the bloc enforces regulations like the Digital Services Act and Digital Markets Act, intended to limit the power of major American technology companies.

- President Trump previously halted trade negotiations with Canada in response to its digital services tax. Soon after, Canada walked back the tax.

- President Trump Suggests Potential New Tariffs on China Over Magnet Dispute: On August 25, President Trump mentioned the possibility of duties as high as 200% if China does not export more rare earth magnets to the United States.

- China produces 90% of the world’s rare earth magnets—a critical component of semiconductor chips, MRI machines, aerospace systems, and more.

- China has eased some export restrictions on its rare earth magnets in recent months. Still, these exports remain a major area of negotiation ahead of November 10, when the extended U.S.-China tariff truce is set to conclude.

- President Trump Announces Potential Furniture Tariffs: On August 22, President Trump announced a “major tariff investigation on furniture” that would conclude within 50 days. He did not provide specifics on duty rates or a timeline for implementation.

- U.S. and EU Announce Framework Trade Agreement: On August 21, the U.S. and the EU published a framework agreement on “reciprocal, fair, and balanced trade,” which establishes the key provisions and goals of a future trade agreement that will be negotiated by both parties. Terms include:

- EU goods will be subject to the higher of either the applicable Most Favored Nation (MFN) duty rate or a 15% duty rate, composed of an MFN tariff and a reciprocal tariff. EU exports of unavailable natural resources (including cork), aircraft and aircraft parts, and generic pharmaceuticals and their precursors will be subject only to the applicable MFN tariff.

- Tariffs on EU pharmaceuticals, semiconductors, and lumber will not exceed 15%.

- Once the EU reduces tariffs on American goods, the U.S. will lower its tariffs on EU automobiles and auto parts from 27.5% to 15%.

- The EU will remove tariffs on U.S. industrial goods while expanding preferential market access for a wide range of U.S. seafood and agricultural goods.

- U.S. Department of Commerce Initiates Investigation into Wind Turbines: On August 13, the U.S. Department of Commerce launched a Section 232 probe into wind turbines and their parts. The results may lay the groundwork for new tariffs on wind components.

- Other Tariff and Trade Updates:

- Effective yesterday (August 27), India is subject to an additional 25% blanket tariff. Depending on shipment departure and arrival dates, some Indian-origin goods face an effective duty rate of 50%.

- The de minimis exemption is set to expire for all U.S. trade partners tomorrow (August 29), at which point low-value goods (i.e., shipments valued at or under $800) will face applicable duties based on their country of origin. To learn how these duties will be assessed, visit our live blog.

- Last week, the U.S. expanded its scope of steel and aluminum tariffs, adding 407 HTS codes to its list of covered “derivative” products. This expansion impacts many key product categories, including consumer packaged goods, household and industrial products, heavy industry and transport-related goods, chemicals and coatings, and energy and infrastructure products. Check out our live blog to learn what this expansion means for compliance, landed costs, and operational complexities.

Calculate and analyze your real-time tariff and landed cost impacts using the Flexport Tariff Simulator.

Ocean

TRANS-PACIFIC EASTBOUND (TPEB)

- Capacity and Demand:

- As Golden Week approaches, demand is not projected to see a significant increase. Some reports indicate that a “pull forward” of shipments earlier this year to beat potential tariffs has resulted in a quiet summer and may lead to a subdued fall. Overall, the market is not seeing a big upsurge in volume.

- Volumes may be impacted by potential furniture tariffs, with President Trump announcing an investigation into furniture imports that will conclude in the coming months.

- September capacity is at 80%-90% of normal levels. Space for shipments remains readily available; demand has not caught up to available capacity.

- Equipment:

- Equipment availability has improved slightly since late July. Equipment shortages remain a primary concern for carriers like CMA and HMM, while other carriers are experiencing better conditions.

- Freight Rates:

- The Peak Season Surcharge (PSS) was removed from the fixed market for the month of August, and through the middle of September. Some carriers have announced a PSS for September 15.

- Carriers have announced a September 1 General Rate Increase (GRI), with an $800-900 increase from current rate levels in August. However, implementation remains uncertain, given overcapacity and softening demand in the market.

FAR EAST WESTBOUND (FEWB)

- Capacity and Demand:

- September blank sailings are expected to reduce weekly capacity by about 10% in the first half of the month.

- Congestion at destination ports remains an issue, and will result in extended transit times in the coming weeks.

- From origin ports, space availability has improved since August and equipment supply has returned to normal. However, we still recommend booking two to three weeks ahead of intended departure.

- Ahead of the traditional pre-Golden-Week demand surge, we strongly advise securing space as early as possible.

- Freight Rates:

- The Shanghai Containerized Freight Index (SCFI) continued to decline last week, dropping to $1,668 per TEU. This marks the SCFI’s fourth week of continuous decline.

- Although September blank sailings will reduce overall capacity, early factory closures before Golden Week will put pressure on carriers to fill vessels. This is likely to gradually lower freight rates.

- On the demand side, volumes have remained relatively stable. The decrease following the traditional peak has not been significant, which could help slow down the pace of rate declines in September.

TRANS-ATLANTIC WESTBOUND (TAWB)

- Capacity and Demand:

- Antwerp: Heavy congestion continues, with yard utilization still exceeding 90% and dwell times at approximately seven days.

- Rotterdam, Hamburg, Bremerhaven: Ports are seeing 75–95% yard utilization and vessel delays of two to three days.

- South Mediterranean (Piraeus, Genoa, Valencia): Heavy congestion continues, with vessel delays of three to six days.

- Equipment:

- Shortages persist in Austria, Slovakia, Hungary, Southern/Eastern Germany, and Portugal.

- Freight Rates:

- Demand is firm, with stable load factors.

- Spot rates from North Europe to the U.S. East Coast are at ~$1,900–$2,000/FEU.

- PSSs have been deferred, with rate extensions through September in North Europe, the East Mediterranean, and the West Mediterranean. Book four to five weeks ahead.

INDIAN SUBCONTINENT TO NORTH AMERICA

- Capacity and Demand:

- Capacity to the U.S. East Coast is decreasing heading into September. Carriers are announcing more blank sailings in response to softening demand from India in light of the additional 25% tariff that was implemented yesterday (August 27).

- Capacity to the U.S. West Coast is widely available, given continued oversupply impacting major TPEB services that move cargo from the Indian subcontinent to the U.S. West Coast. Some core feeder services on this route may reduce capacity in the coming weeks following a decline in demand from India.

- Freight Rates:

- For cargo moving to the U.S. East Coast, rate levels are decreasing slightly as we head into September.

- For cargo moving to the U.S. West Coast, oversupply on core TPEB lanes has continued to keep the market soft.

- If the 25% tariff (implemented yesterday) remains in place, we expect to see a continued softening in demand from India.

Air

- TPEB:

- Northern China: Demand is soft, even at month’s end. Rates are declining.

- Southern China: Demand is also soft, across both traditional cargo and ecommerce.

- Taiwan: Demand remains strong heading to the U.S. West Coast; rates are holding.

- Vietnam: The market remains tight and rates are high ahead of the long local holiday. We highly recommend placing bookings five or more days ahead.

- Indian Subcontinent:

- India: Despite previous optimism about a potential agreement between the U.S. and India regarding the new 25% blanket tariff implemented yesterday (August 27), there hasn’t been any new progress quickly driving rates out of India. Several airlines announced that they would not be taking in urgent cargo before August 27, as demand skyrocketed in the past week. We’re expecting some backlogs and congestion at terminals until early next week; advance bookings are highly encouraged.

(Source: Flexport)

Please reach out to your account representative for details on any impacts to your shipments.

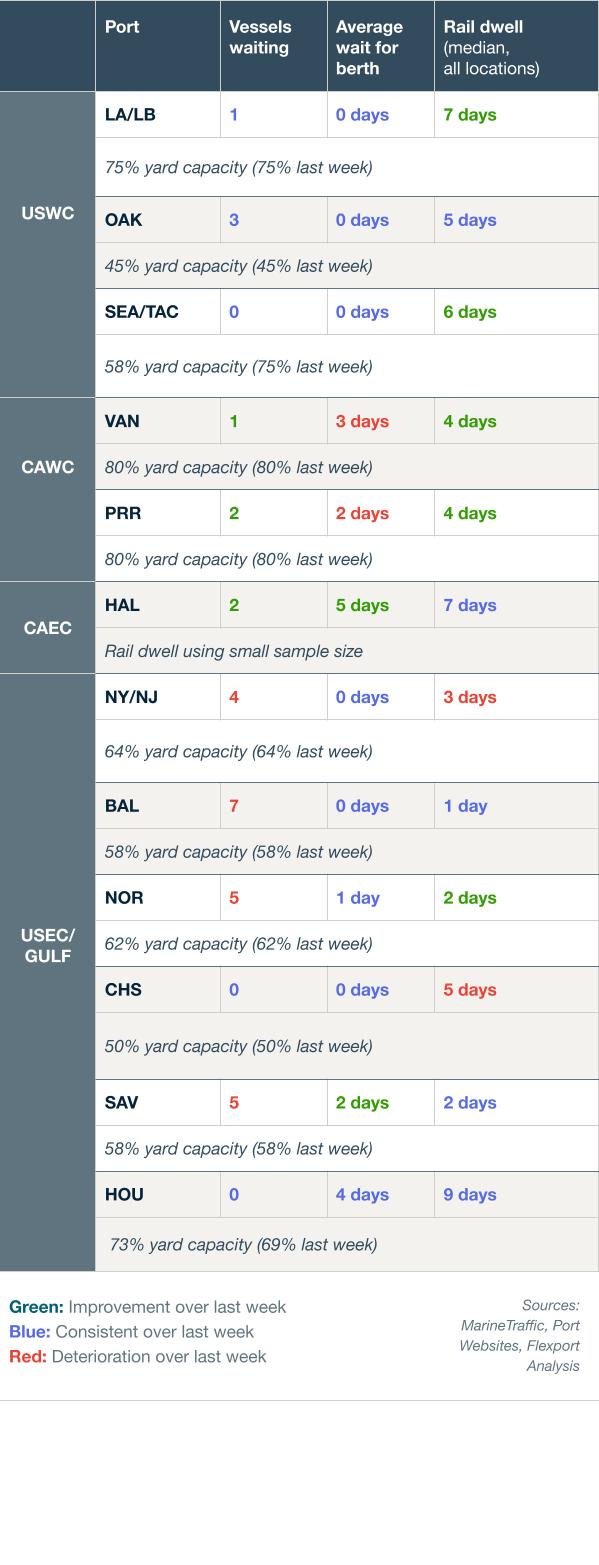

North America Vessel Dwell Times

Webinars

North America Freight Market Update Live

Thursday, September 11 @ 9:00 am PT / 12:00 pm ET

Tariff Trends 2025: Expert Insights on the New U.S. Customs Landscape (Section 232 Focus)

Watch On-Demand

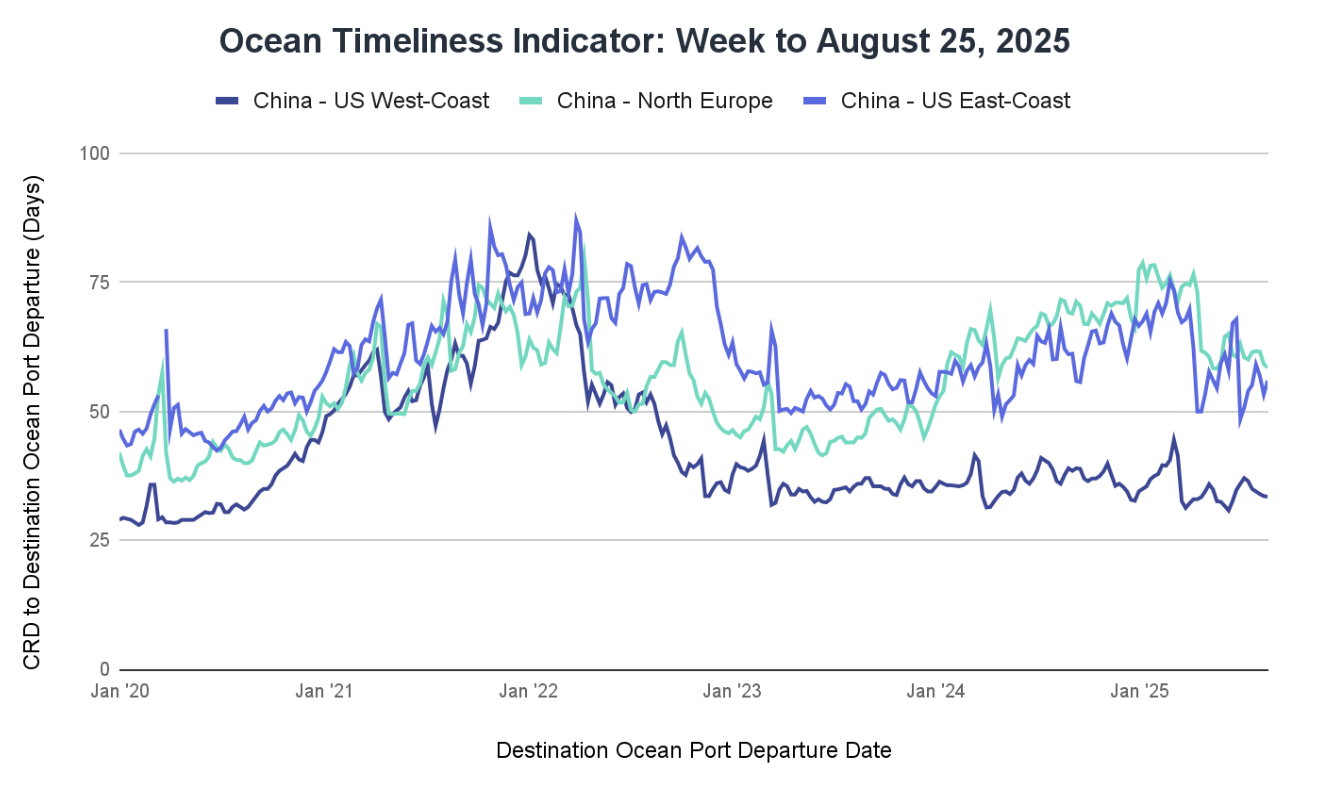

Ocean Timeliness Indicator

Transit times from China to the U.S. West Coast, North Europe, and the U.S. East Coast all experienced reductions, with the most significant decrease observed on the U.S. East Coast route.

Week to August 25, 2025

Transit time from China to the U.S. West Coast decreased by 0.1 days, falling from 33.6 to 33.5 days. The China to North Europe route saw a 0.7-day decrease, moving from 59.2 to 58.5 days. Meanwhile, transit time from China to the U.S. East Coast decreased by 3.6 days, falling from 56.9 to 53.3 days.

See the full report and read about our methodology here.

About the Author

Related content

![White House GettyImages-603224136 (1)]()

Blog

Live Updates: Trump Administration Tariffs, Trade Policy Changes, and Impacts on Global Supply Chains

![GettyImages-1411182583 1199x800]()

Blog

CBP’s Latest Guidance on Reporting Country of Smelt and Cast for Section 232 Aluminum Tariffs

更多

![WarehouseGettyImages-535667233]()

Global Logistics Update

U.S. and Taiwan Finalize Trade Deal; FEWB Spot Rates Soften Amid Lunar New Year Lull

![Ocean Port GettyImages-1083936322 (1)]()

Global Logistics Update

EU to Vote on Modified U.S. Trade Deal; Ex-Asia Demand Tapers Off Ahead of Lunar New Year

![Air GettyImages-1343405900]()

Global Logistics Update

U.S. to Cut Tariffs on India; TPEB and FEWB Carriers Plan Upcoming Blank Sailings