Back to Global Logistics Update

Global Logistics Update

25% Tariffs on Foreign Cars; FEWB & TAWB: Market Shake-up & Delays

North America vessel dwell times and other updates from the global supply chain | May 17, 2023

Global Logistics Update: March 27, 2025

Trends to Watch

Talking Tariffs:

We launched the Flexport Tariff Simulator. Estimate and forecast tariffs and landed costs for each shipment, all based on real-time data and the latest rates and regulations.

- Yesterday, President Donald Trump announced a 25% tariff on all cars imported into the U.S., set to take effect at 12:01a.m. ET on April 3, 2025. The tariff will apply to passenger vehicles, light trucks, and auto parts, including American brands assembled overseas. Nearly half of all vehicles sold in the U.S. are imported.

- On Monday (March 24, 2025), President Donald Trump issued an executive order imposing a 25% tariff on all countries that buy oil or gas from Venezuela, effective April 2. This will be added on top of the existing tariffs.

- China and the U.S. are among the biggest buyers of Venezuelan oil — representing nearly 63% of the total crude oil produced per day. Additionally, India, Spain, Brazil, and Turkey are regular importers of Venezuelan oil as well.

- While the April 2 deadline is looming for a number of levies to take effect, President Donald Trump stated that not all tariffs will be announced that day and that “a lot of countries” may receive exemptions.

- "I'll probably be more lenient than reciprocal, because if I was reciprocal, that would be very tough for people," Trump said Tuesday.

- Follow [our live blog](https://www.flexport.com/blog/what-president-trumps-2024-u-s-election-win-means-for-global-trade-and/?utm_source=flexport&utm_medium=email&utm_campaign=subm-freight market update &utm_content=32625) for the latest updates on trade.

Ocean: Trans-Pacific Eastbound (TPEB)

- Capacity and Demand:

- March demand has remained stagnant, showing no growth since after the Chinese New Year (CNY). Forecasted demand has not met expectations, or has not materialized as projected.

- Capacity: Shipping capacity remains healthy, with deployment staying above 80% from the rest of March into April.

- Equipment:

- Ample equipment supply is available across most origin gateways, and no major shortages are expected.

- Freight Rates:

- Floating market rates: There has been a slowdown in floating market rates this week, with rates stabilizing at current levels.

- April GRI and rate stabilization: Carriers have announced their General Rate Increase (GRI) for April.

- PSS removal: The Peak Season Surcharge (PSS) has been removed by most carriers for the remainder of March.

Ocean: Far East Westbound (FEWB)

- Capacity and Demand: For early April, only one voyage cancellation has been announced so far, indicating that the oversupply situation is likely to persist. Since mid-March, booking requests in the market have increased, accompanied by new bid submissions, indicating a gradual recovery in demand.

- Vessel Accident: According to a report from the PA Alliance, the FE4 voyage ONE INTEGRITY 006W experienced a fire on board while sailing from Cai Mep to Singapore. The 24,000-TEU vessel operates on routes from PRE/PRS to RTM/HAM. This incident could lead to significant delays for SEA transshipment bookings and shipments already on board in Singapore.

- Freight Rates:

- The Week 12 Shanghai Containerized Freight Index (SCFI) saw a slight decrease, indicating that freight rates will remain steady through the end of March. The April GRI implementation was unsuccessful, with most carriers postponing the planned increase to late April and lowering the proposed rate adjustment.

- Additionally, more cargo is being loaded in late March or planned for early April, which will help reduce further drops in FAK rates. However, there are still no signs of a significant rate increase in the short term.

Ocean: Trans-Atlantic Westbound (TAWB)

- Capacity and Demand: Blank sailings were reduced in March. In April, we expect blank sailings in Southern Europe, primarily due to congestion and vessel delays in the region. Ports experiencing congestion include Piraeus, Mersin, and Valencia, leading to service delays.

- Equipment: Equipment shortages persist in parts of Central Europe, particularly in Austria, Slovakia, Switzerland, Hungary, and Southern/Eastern Germany. Carrier haulage is recommended for these origins. In the East Mediterranean, Mersin is beginning to face equipment challenges.

- Freight Rates: The PSS implementation for exports from Spain, Italy, Portugal, and Southern France, initially planned for April 1st, has been postponed by some carriers to April 14th and 15th due to high demand and vessel delays. The North Europe PSS has been canceled, and there is no update for a PSS in the East Mediterranean as demand remains flat.

Air Freight Update (March 10 - March 16, 2025 Week 11):

- Global volume trends

- Worldwide air cargo tonnages rose +1% week-on-week (WoW) and are now +3% year-on-year (YoY). The rise was led by Central and South America (+4%) and the Asia-Pacific (+3%), while the Middle East and South Asia (MESA) saw a -4% WoW drop due to Holi- and Ramadan-related slowdowns.

- Asia-Pacific rebound

- Tonnages from the Asia-Pacific surged +13% to Europe and +10% to North America on a two-week-on-two-week (2Wo2W) basis. WoW, tonnages to Europe grew +7%, with notable gains from South Korea (+18%), Taiwan (+13%), and Vietnam (+9%). Tonnages to the USA also rose +5% WoW.

- Rates movements—Asia-Pacific focus

- Asia-Pacific to Europe: Rates held at $3.92/kg (flat WoW), but +16% YoY overall, including +8% from China and +18% from Japan.

- Asia-Pacific to USA: Rates were $4.91/kg (down -1% WoW, up +11% YoY), with big WoW hikes from China and South Korea (+15%), but drops from Japan (-8%) and Vietnam (-11%).

- Global pricing

- Average global air cargo rates rose +3% WoW to $2.37/kg, now +2% above last year’s level, driven by both spot and contract rate increases.

- Implications for logistics professionals

- Expect tighter capacity and upward pressure on rates—especially from the Asia-Pacific—driven by strong post-Lunar-New-Year recovery. Shippers should consider booking early and revisiting budget forecasts if necessary.

Source: worldacd.com

Please reach out to your account representative for details on any impacts to your shipments.

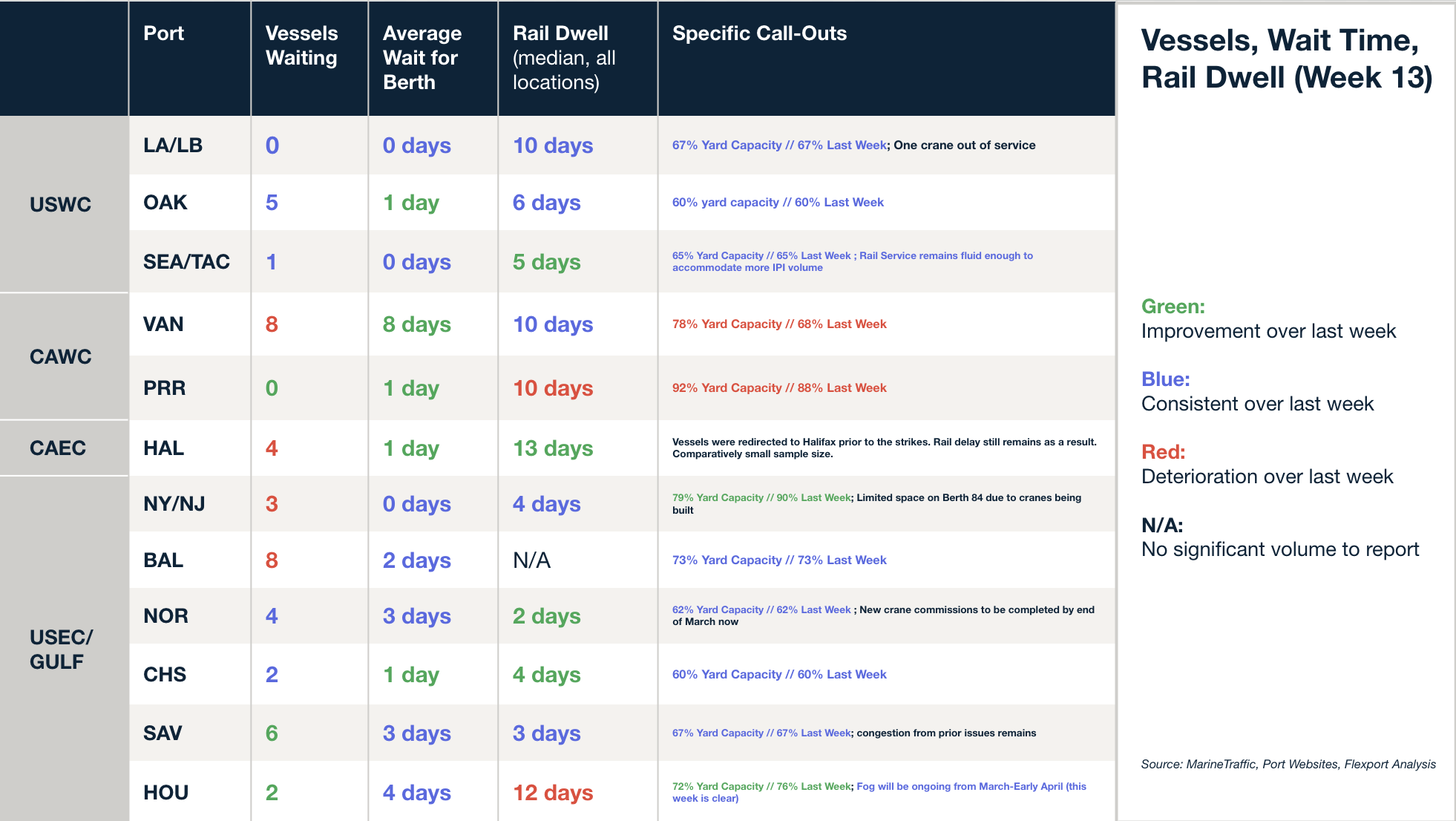

North America Vessel Dwell Times

About the Author

Related content

更多

![Compliance GettyImages-520614727]()

Global Logistics Update

Nations Brace for Aug. 1 Reciprocal Duties; FEWB Faces Blank Sailings and Backlogs

![GettyImages-1152525211]()

Global Logistics Update

U.S. Announces August 1 Reciprocal Duty Rates; Demand Remains Steady Across Most Trade Lanes