Global Logistics Update

U.S. and China Announce a Temporary Trade Deal; TPEB Services Start to Resume

North America vessel dwell times and other updates from the global supply chain | May 17, 2023

Global Logistics Update: May 15, 2025

Trends to Watch

Talking Tariffs

We launched the Flexport Tariff Simulator. Estimate and forecast tariffs and landed costs for each shipment, all based on real-time data and the latest rates and regulations.

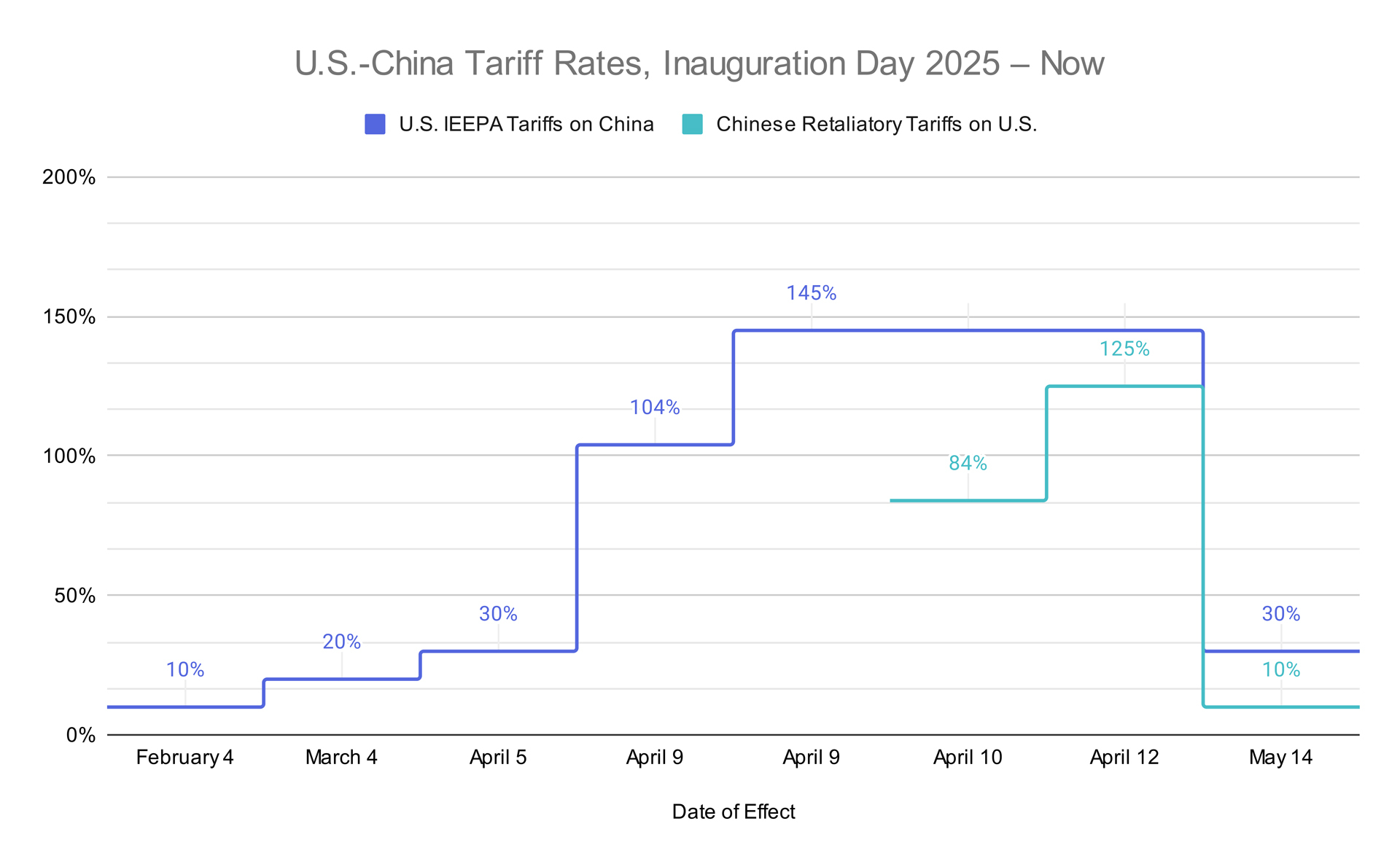

- U.S. Reduces 125% IEEPA Reciprocal Tariffs on Chinese Goods to 10%: On Monday, May 12, following a weekend of in-person negotiations in Switzerland, President Trump issued an executive order:

- Reduces IEEPA reciprocal tariffs on Chinese goods from 125% to 10% for 90 days, effective May 14 through August 11. On August 12, the IEEPA reciprocal tariff rate will increase to 34%.

- Maintains IEEPA fentanyl tariffs on Chinese goods at 20%, resulting in an effective total IEEPA tariff rate of 30% during this 90-day period, and 54% thereafter.

- Reduces tariff rates on postal items valued at $800 or less from 120% to 54%, while maintaining the option to pay a $100 flat fee instead. The increase to a $200 flat fee scheduled to take effect on June 1 has been redacted. Check out our blog for details on new fees, special provisions and requirements, and changes to consumer delivery procedures for postal shipments from China/Hong Kong.

- China also reduced its retaliatory tariff rate on U.S. goods from 125% to 10%.

- The Latest on Other Reciprocal Tariffs:

- The 10% IEEPA reciprocal tariff on the U.K. will be in place indefinitely, per last Thursday’s trade deal.

- The 10% IEEPA reciprocal tariff on all other U.S. trade partners remains in effect until July 9 at 12:01 a.m. ET. After that, country-specific reciprocal tariffs will be implemented.

- Any HTS in Annex II is exempt from reciprocal tariffs, regardless of the country of origin. As of April 16, 2025, semiconductor products are also excluded from reciprocal tariffs.

Ocean

TRANS-PACIFIC EASTBOUND (TPEB)

- Capacity and Demand:

- The anticipated surge in demand ex-China due to the temporary U.S.-China trade deal, combined with existing backlogs and the lead-up to peak season, strongly suggests a significant increase in shipping volumes on the TPEB route throughout the rest of Q2.

- Carriers are in the process of bringing back capacity, with changes expected to begin at the end of May and a greater capacity increase in June. Week 20 capacity on the TPEB was 20% below standard levels—a slight decrease compared to previous weeks. However, capacity is forecasted to improve in Weeks 21 and 22: 16% and 10% below standard levels, respectively.

- To address the immediate demand surge, some carriers might explore extra loaders. Still, available vessel space on the TPEB may not be able to meet the anticipated spike in demand.

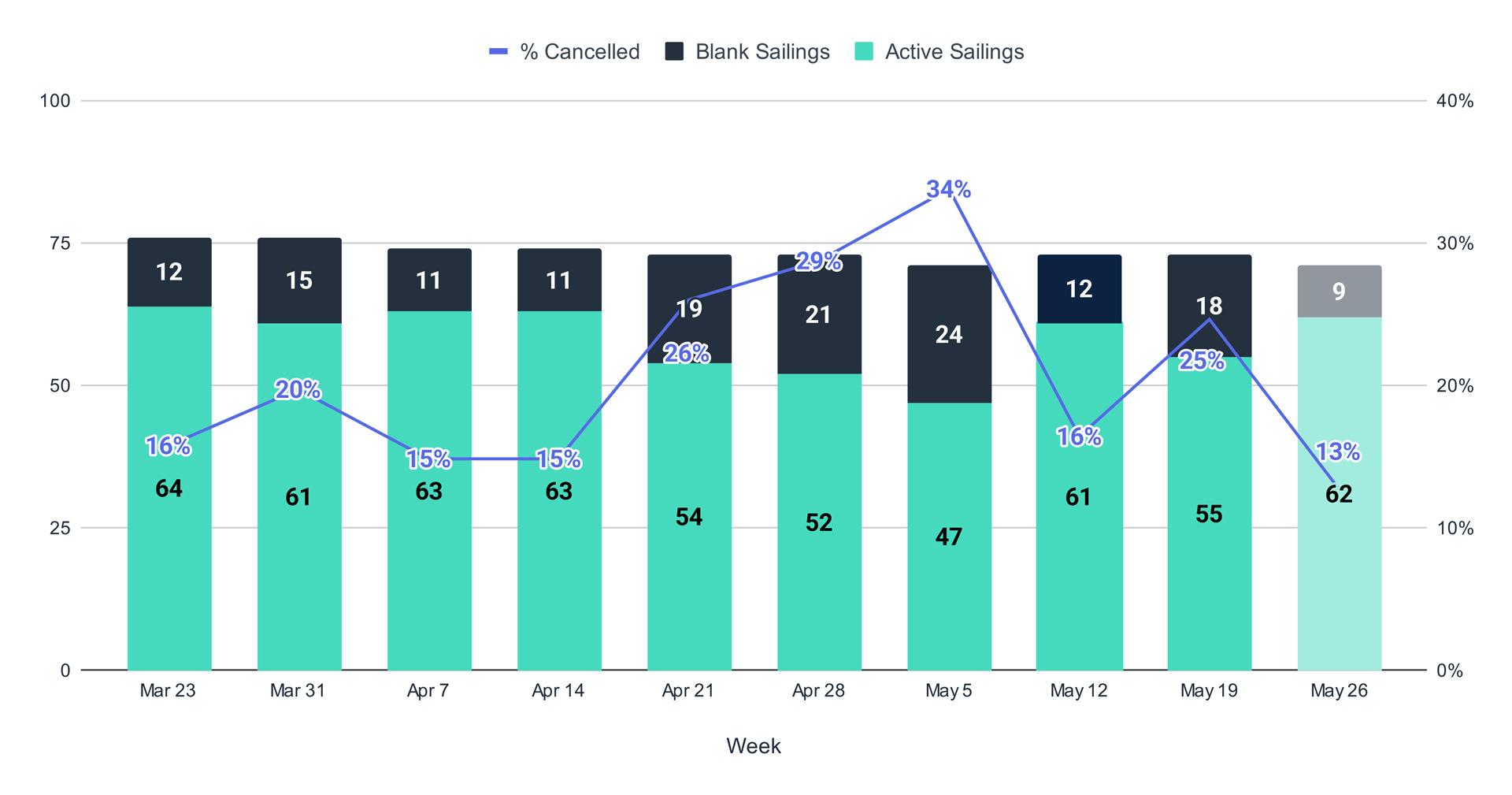

- Blank Sailings, China to the U.S.: This week (May 12), we saw a temporary decrease in blank sailings, followed by a 25% cancellation rate (+9% WoW) the following week. However, in light of the temporary U.S.-China trade agreement, blank sailings are forecasted to decrease again the week of May 26, with a projected cancellation rate of 13%—the fewest blank sailings since late March. In addition, carriers may further ingest withdrawn capacity, depending on how quickly demand recovers.

Two service loops are already scheduled to resume the week of May 26. See the updated table below, and check out our blog post for more details.

Table 1: Suspended Transpacific Eastbound Service Loops (Updated May 13, 2025)

| Carrier / Alliance | Service Loop | Suspension Period |

|---|---|---|

| Ocean Alliance | PRX / CP1 / PCS1 / PRX / AAS2 | Week 17 - 26 |

| Ocean Alliance | SEA3 / PSX | Week 18 - 23 |

| Ocean Alliance | CPS / AAC2 / HBB / PCN3 | Will resume Week 22 |

| Ocean Alliance | CBX / ECC3 / AWE7 / CBX | Week 16 - 24 |

| Mediterranean Shipping Company | ORIENT | Week 16 until further notice |

| ZIM | ZX2 | Will resume Week 22 |

| Premier Alliance | PN4 | Scheduled to begin in May, suspended until further notice |

| Premier Alliance | PS5 | Scheduled to begin in May, suspended until further notice |

| Mediterranean Shipping Company / ZIM | PELICAN / ZSL | Week 19 until further notice |

| Mediterranean Shipping Company / ZIM | EMPIRE / ZNS | Week 20 until further notice |

- Equipment: Equipment availability is currently sufficient. Container shortages aren’t an immediate concern on this lane, though the situation is fluid and warrants continued monitoring.

- Freight Rates: Rising spot rates are expected, given confirmation of the May 15 GRI and the announced $3,000 GRI for June 1, specifically on the floating market for the TPEB. Driven by the anticipation of higher volumes, Peak Season Surcharges (PSSs) have been announced for the fixed market, some starting as early as mid-May and as late as June 1.

FAR EAST WESTBOUND (FEWB)

- Capacity and Demand:

- Following Labor Day blank sailings, the three major alliances have not announced any additional blank sailings. Full capacity deployment is expected over the next 3-4 weeks.

- But due to earlier capacity removal, particularly for Southeast Asia transshipment routes, last-call ports of loading (POLs) in Southeast Asia face a ~30% capacity reduction in Week 21. Beyond Week 21, overall weekly capacity remains stable at 310K–320K TEU.

- The European market is seeing a seasonal recovery in consumer demand, supported by interest rate cuts in key Asian export economies, which should boost export volumes in the coming weeks. European retailers continue to restock for peak season. However, short-term FEWB demand may be subdued as manufacturers prioritize urgent U.S. shipments after tariff reductions, diverting volume away from the FEWB.

- Tariff Impacts on EU Trade:

- The recent U.S.-China tariff adjustments are expected to trigger a surge in Trans-Pacific trade volumes, as factories shift production to meet increased Trans-Pacific orders over the next 3-4 weeks. This could temporarily reduce FEWB shipments due to constrained manufacturing capacity.

- Additionally, as more cargo shifts back to the U.S. trade lane, vessel capacity previously diverted to Europe may be reallocated to Trans-Pacific routes again, easing oversupply pressure on EU lanes.

- The tariff adjustments should slow the decline in EU freight rates by mitigating excess capacity.

TRANS-ATLANTIC WESTBOUND (TAWB)

- Capacity and Demand: Congestion persists at the Ports of Piraeus, Genoa, and Valencia in the Mediterranean, and in Hamburg, Rotterdam, Antwerp, and London Gateway Port in North Europe. This has led to delays and is negatively affecting schedule reliability.

- Equipment: Equipment shortages persist in parts of Central Europe, particularly in Austria, Slovakia, Switzerland, Hungary, and Southern/Eastern Germany. Carrier haulage is recommended for these origins. Mersin and Aliaga in Turkey and Lisbon in Portugal are facing equipment shortages, and carriers are carrying out empty repositions to support demand.

- Freight Rates: The peak in demand anticipated by carriers has not come to fruition. Vessel utilization is good but not overbooked, forcing carriers to reconsider PSS implementation.

- North Europe: Some carriers have postponed their May PSS until June; others have postponed it until further notice.

- West Mediterranean: The PSS has been postponed.

- East Mediterranean: Carriers have postponed their May PSS until June.

INDIAN SUBCONTINENT TO NORTH AMERICA

- Capacity and Demand:

- Demand remains stable, with carriers reporting high utilization on direct services from the region. No decline has been noted, despite the ongoing conflict between Pakistan and India.

- Space is generally available on most services, but any surge in demand could lead to demand outstripping capacity. Space from Pakistan is particularly tight, as carriers are rerouting services and launching new feeder services due to India’s restrictions, which prohibit vessels carrying Pakistani cargo from berthing in India.

- Freight Rates: Rates are expected to rise in the second half of May due to sustained demand and anticipated blank sailings. These cancellations stem from insufficient vessels to maintain weekly sailings for some services.

Air

WEEK 18: APRIL 28 - MAY 4, 2025

- Tonnages Down -3% Globally WoW: -11% was driven by the Asia-Pacific, especially ex-China and Hong Kong due to Labor Day, Japan’s Golden Week, and the expiration of de minimis in the U.S. for Chinese-origin goods on May 2. Ex-Japan volumes alone fell -45% WoW.

- Trans-Pacific Flows Hit the Hardest: China to the U.S. saw a -14% WoW drop, versus China to Europe’s -3% drop. This suggests the de minimis policy shift is already disrupting ecommerce-driven volumes; dozens of freighter services have reportedly been cancelled or rerouted.

- Rates Stable Overall at $2.40/kg: But Asia-Pacific rates were up +3% WoW due to a "mix effect" from the intra-Asia volume plunge. Excluding intra-Asia, APAC rates actually declined -1% WoW.

- Spot Rates Diverging: China–U.S. spot rates fell -9% WoW to $3.85/kg, their fourth weekly drop. Meanwhile, China–Europe rates slipped just -4% to $3.97/kg, showing pricing resilience on westbound lanes.

- Temporary U.S.-China Tariff Deal: The 90-day trade deal will cut duties sharply (145% → 30% U.S., 125% → 10% China), likely boosting Trans-Pacific air freight volumes in the short term. That said, the 90-day limit means the long-term outlook remains uncertain.

Source: worldacd.com

Please reach out to your account representative for details on any impacts to your shipments.

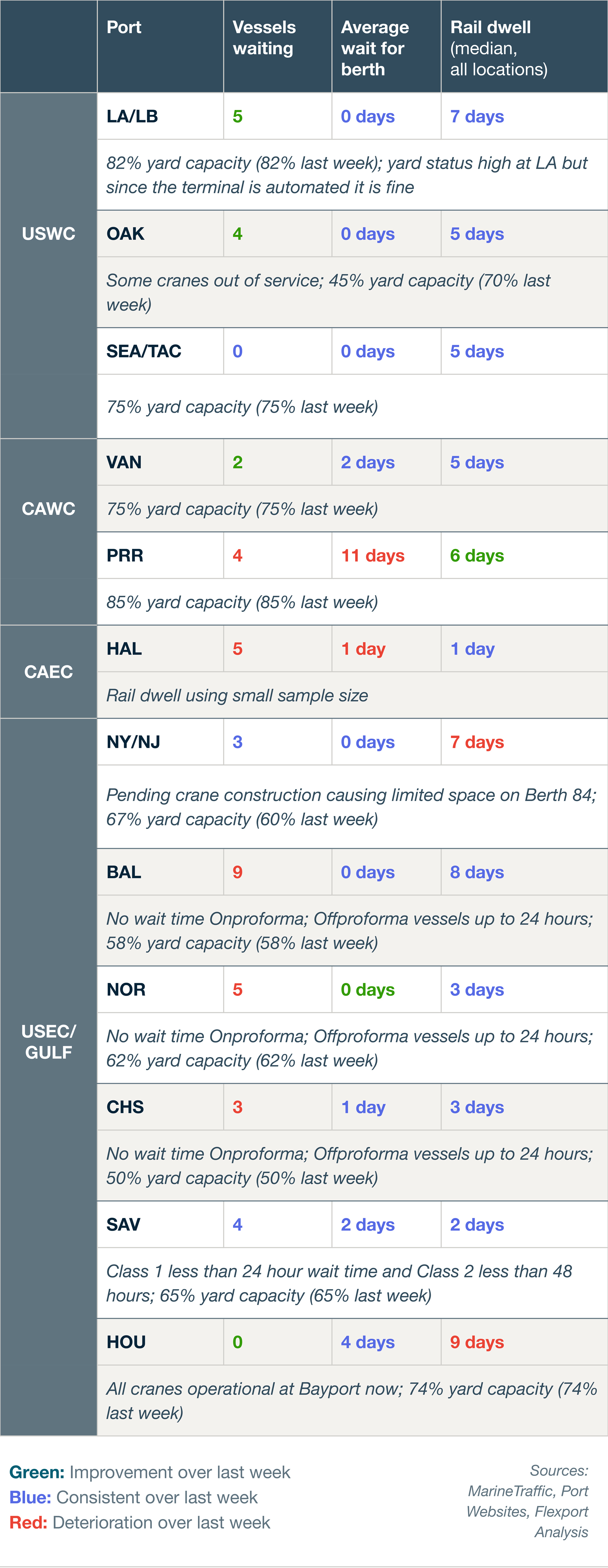

North America Vessel Dwell Times

Upcoming Webinars

European Freight Market Update Live

Tuesday, May 20 @ 15:00 BST / 16:00 CEST

North America Freight Market Update Live

Thursday, May 22 @ 9:00 am PT / 12:00 pm ET

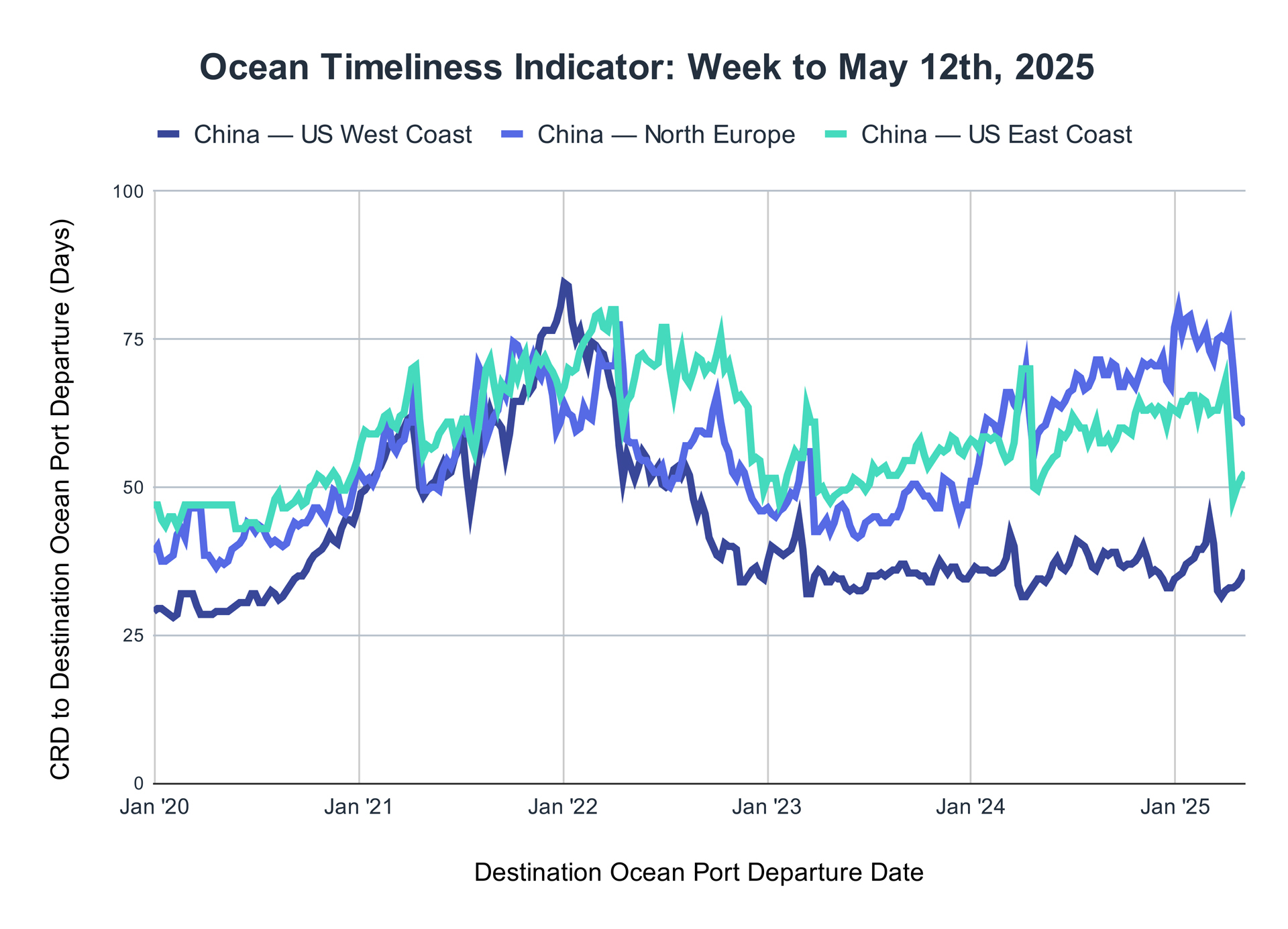

Ocean Timeliness Indicator

The previous week’s pattern continues this week: the Flexport OTI for China to the U.S. West Coast and China to the U.S. East Coast showed a small uptick, while China to North Europe decreased.

Week to May 12, 2025

The Ocean Timeliness Indicator (OTI) showed minor fluctuations again this week, with China to the U.S. West Coast increasing from 34.5 to 36 days and China to the U.S. East Coast increasing from 51.5 to 52.5 days. Meanwhile, China to North Europe fell slightly once again, from 61.5 to 60.5 days.

About the Author

Related content

更多

![WarehouseGettyImages-535667233]()

Global Logistics Update

U.S. and Taiwan Finalize Trade Deal; FEWB Spot Rates Soften Amid Lunar New Year Lull

![Ocean Port GettyImages-1083936322 (1)]()

Global Logistics Update

EU to Vote on Modified U.S. Trade Deal; Ex-Asia Demand Tapers Off Ahead of Lunar New Year

![Air GettyImages-1343405900]()

Global Logistics Update

U.S. to Cut Tariffs on India; TPEB and FEWB Carriers Plan Upcoming Blank Sailings