Global Logistics Update

CBP Excludes Feeder Vessels from Reciprocal Tariff Exceptions; TPEB Capacity Improves

North America vessel dwell times and other updates from the global supply chain | May 17, 2023

Global Logistics Update: May 22, 2025

Trends to Watch

Talking Tariffs

We launched the Flexport Tariff Simulator. Estimate and forecast tariffs and landed costs for each shipment, all based on real-time data and the latest rates and regulations.

- Customs and Border Protection (CBP) Provides Clarification on Feeder Vessel Eligibility for Reciprocal Tariff In-Transit Exceptions: On May 15, 2025, U.S. CBP clarified that goods on feeder vessels do not qualify for in-transit exceptions to IEEPA reciprocal tariffs, even if the cargo is loaded before the cutoff date.

- To qualify for the reciprocal in-transit exemption, the shipment must have been loaded onto its final mode of transit—i.e., the final ocean vessel heading to the cargo’s port of destination in the U.S.—before April 5, 2025.

- To qualify for the baseline 10% reciprocal duty rate, shipments originating from China, Hong Kong, or Macau must have been loaded onto its final ocean vessel by April 9, 2025.

- Even if a shipment meets the in-transit exception requirements based on departure date, the goods must arrive and be cleared through Customs before May 27, 2025.

- Based on this clarification, fewer entries will qualify for reciprocal in-transit exceptions. Many importers will be subject to higher duties—including retroactive duties that accompany any changes to filed entries.

- Importers have the option to file a protest with CBP. Flexport’s trade advisory team can help—reach out to your account manager or advisory@flexport.com for assistance.

- Get additional details from our latest blog post.

- The Latest on De Minimis and T11:

- In light of the May 2 expiration of de minimis for Chinese-origin goods, T11 entries (informal entries) have been modified to apply to entries valued at $2,500 or less. For shipments subject to IEEPA or Section 301 tariffs, the previous shipment value limit for T11 entries was $250.

- Per last Monday’s executive order, low-value shipments sent via the postal system are subject to simpler declarations, with the choice of either a 54% duty rate or a $100 flat fee to be determined by the postal carrier. Carriers will collect duties—paid by the consumer in advance, or upon pickup or delivery—and remit them to CBP.

- Check out our blog for details on the latest fees for low-value postal shipments, entry requirements and carrier responsibilities, and consumer delivery procedures.

- The Latest on Reciprocal Tariffs:

- Chinese-origin goods with a time of entry on or after May 14, 2025, are subject to a 10% reciprocal tariff until August 11, 2025. On August 12, the reciprocal duty rate will increase to 34%.

- Goods originating from the U.K. are subject to an indefinite 10% reciprocal tariff.

- Goods from other countries of origin are subject to a 10% reciprocal tariff until July 9, 2025.

- Any HTS in Annex II is exempt from reciprocal tariffs, regardless of the country of origin. As of April 16, 2025, semiconductor products are also excluded from reciprocal tariffs.

Ocean

TRANS-PACIFIC EASTBOUND (TPEB)

- Increased Demand:

- TPEB demand is increasing significantly and is expected to continue throughout Q2 due to the temporary reduction of U.S. tariffs on Chinese-origin goods, and the upcoming traditional peak season.

- Given increased demand, vessel capacity is being booked up. Shippers are advised to book four weeks in advance and use premium options if urgency is a priority. Reach out to your Flexport representative for more information on premium options.

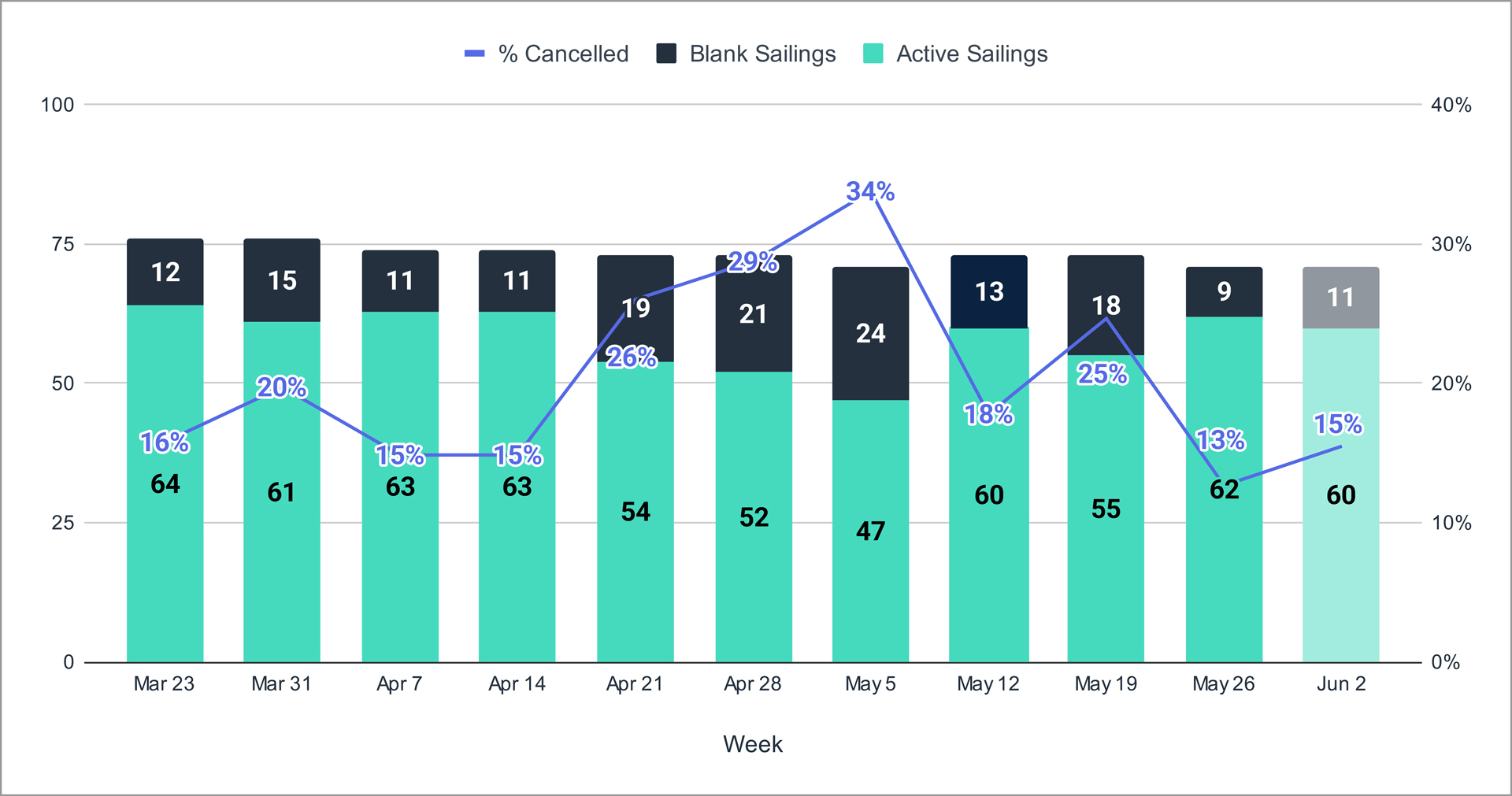

- Increased Capacity and Service Resumptions:

- Carriers are bringing back capacity to meet increased demand starting at the end of May, with even more capacity expected in June.

- This week (Week 21), TPEB capacity is 10% below standard levels—a 13% improvement since Week 19. Capacity is forecasted to improve further next week, projected at 8% below standard levels.

- Cancellations were at 25% this week. However, blank sailings are expected to decrease next week (May 26), with a projected 13% cancellation rate—the fewest since late March.

- Blank sailings are expected to loosely remain at that level in the first week of June, with a projected 15% cancellation rate.

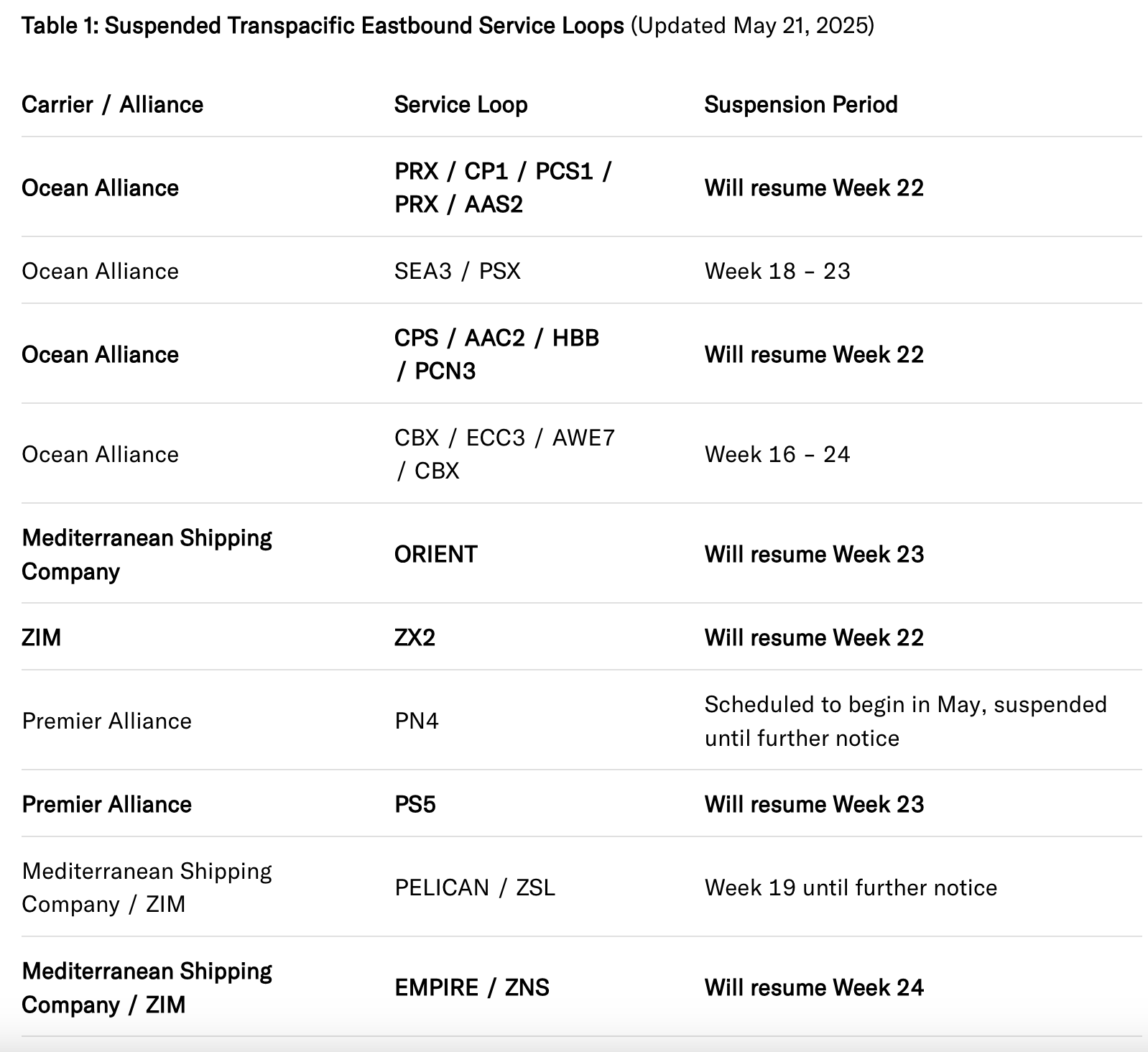

- Six previously suspended service loops are now scheduled to resume—some as early as next week (Week 22). See the updated table below, and read our blog for more details.

- Carriers may further ingest withdrawn capacity, depending on how quickly demand recovers. Carriers are also exploring extra loaders, mostly to Los Angeles/Long Beach (LA/LGB).

- Even with these actions, available vessel space on the TPEB may not be able to meet anticipated demand.

- Equipment: Equipment availability remains sufficient. Container shortages aren’t an immediate concern, though the situation is fluid and warrants continued monitoring.

- Freight Rates:

- Given the May 15 General Rate Increase (GRI) and the $3,000 GRI announced for June 1, expect rising spot rates—specifically on the TPEB’s floating market.

- With increased booking volumes and capacity crunch, Peak Season Surcharges (PSSs) have been announced for the fixed market. Implementation started in mid-May and will increase June 1 across the trade.

FAR EAST WESTBOUND (FEWB)

- Capacity and Demand:

- Premier Alliance is deploying smaller vessels from late May to early June, but capacity overall remains stable at 310K–320K TEUs per week through the end of May. Week 25—a reduced-capacity week, with 265K TEUs—will bring a capacity decrease of about 17%, impacting shipments with estimated times of departure (ETDs) between June 9 (Shanghai/Ningbo/Qingdao) and June 16 (Yantian/Southeast Asia).

- Port congestion in the Far East—especially in Shanghai and Ningbo—is leading to significant vessel delays.

- Cargo volumes continue to recover steadily, but there is no clear sign of a peak season turning point yet. In Week 19, container throughput in Chinese ports of loading (POLs) reached 6.201 million TEUs—a 5.76% decrease from the previous week. Recent U.S.-China tariff developments are mainly affecting the FEWB on the supply side, with limited impact on demand.

- Demand on the Europe lane continues to follow typical seasonal patterns, with cargo volumes usually rising gradually from April to August. The peak season turning point will depend on Europe’s holiday-related stockpiling, which typically occurs between July and August.

- Equipment: Given the surge in Trans-Pacific cargo in late May, equipment inventory may face challenges, potentially impacting FEWB trade. An equipment shortage could prompt carriers to restrict FEWB space in the coming weeks.

- Freight Rates:

- FEWB rates are expected to move back toward a more sustainable range. Following the cargo rush on the Trans-Pacific trade lane, which had driven expectations for an increase in FEWB rates, the market stopped dropping and is gradually returning to a more rational state.

- Based on current quotes for 40' containers in early June, the Shanghai Containerized Freight Index (SCFI) is projected to see a steep increase by the end of May.

- However, with relatively high capacity still scheduled for the first half of June, it remains uncertain whether the proposed GRI for June will be fully implemented.

TRANS-ATLANTIC WESTBOUND (TAWB)

- Capacity and Demand: Congestion persists at the Ports of Antwerp, Rotterdam, Bremerhaven, and London Gateway in North Europe, and in Piraeus, Genoa, and Valencia in the Mediterranean. This has led to ongoing delays and continues to negatively impact schedule reliability.

- Equipment: Equipment shortages persist in parts of Central Europe, particularly in Austria, Slovakia, Switzerland, Hungary, and Southern/Eastern Germany. Carrier haulage is recommended for these origins. Mersin and Aliaga in Turkey and Lisbon in Portugal are facing equipment shortages, and carriers continue to carry out empty repositions to support demand.

- Freight Rates: The peak in demand anticipated by carriers has not yet taken place.

- North Europe: Carriers have postponed their May PSS until June, while others have postponed it until further notice.

- West Mediterranean: The PSS has been postponed.

- East Mediterranean: Carriers have also postponed their May PSS until June.

INDIAN SUBCONTINENT TO NORTH AMERICA

- Capacity and Demand:

- Demand from the region remains stable. Carriers are reporting that vessels continue to be highly utilized.

- Space out of Pakistan is constrained in light of network changes stemming from the India-Pakistan conflict. Pakistani cargo connects to main liner services through transhipments, whereas Northwest India ports continue on their direct services to the U.S.

- Capacity from India to the U.S. West Coast is constrained due to limited direct services, which are seeing an influx of cargo from Chinese ports of origin along the service string.

- Freight Rates:

- From India, rates are expected to increase amid capacity shifting back to ex-China to U.S. lanes, creating gaps in scheduling that will require blanks.

- Rates will rise to the U.S. West Coast, as the direct service is highly utilized.

- Exports from Pakistan are seeing increases due to additional feeder services being launched in light of the India-Pakistan conflict.

Air

WEEK 19: MAY 5 - MAY 11, 2025

- Global Tonnages Drop -3% (2Wo2W), Led by the Asia-Pacific: Worldwide chargeable weight fell -3% over two weeks, driven by a sharp -8% decline from the Asia-Pacific, especially China-U.S. lanes (-13%). Key factors: the end of the U.S.’s de minimis exemption (May 2), and the Labor Day and Golden Week holidays.

- Rates Continue Slide, -2% (2Wo2W) and -3% YoY: Average global rates declined to $2.34, down -2% vs. two weeks prior and -3% YoY. Pricing pressure came from weaker demand, tariff uncertainty, and falling ocean freight rates. Only North America (+3%) and Europe (+1%) saw week-on-week increases, which were partially due to a post-holiday rebound.

- China-U.S. Air Freight Plummets -27% YoY: Week 19 chargeable weight from China/Hong Kong to the U.S. dropped -10% WoW, after a -14% fall the prior week. Volumes are down -27% YoY— the fourth straight week of a double-digit YoY decline following the end of de minimis for Chinese goods.

- Capacity Tightens, Especially in Asia (-5% 2Wo2W): Global air freight capacity fell -2% over two weeks, led by a -5% drop in the Asia-Pacific due to Golden Week. Europe was the only region with rising capacity (+1%), supporting Trans-Atlantic growth (+6% 2Wo2W) amid tariff-driven front-loading.

- Impact of Temporary U.S.-China Trade Agreement: The temporary U.S.-China trade deal is likely to boost Trans-Pacific air freight volumes in the short term, though the 90-day limit means the long-term outlook remains uncertain.

(Source: WorldACD)

Please reach out to your account representative for details on any impacts to your shipments.

North America Vessel Dwell Times

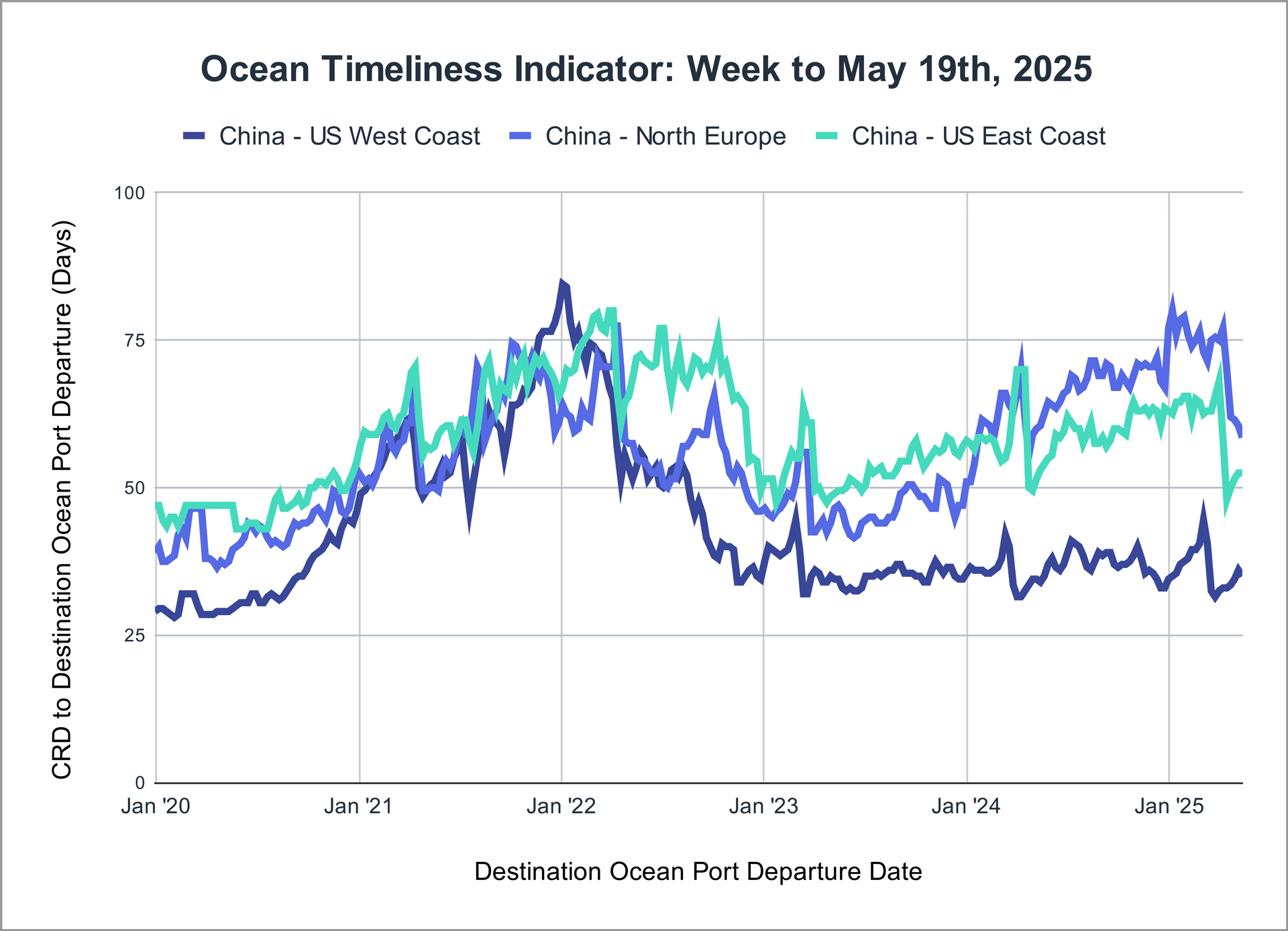

Ocean Timeliness Indicator

This week, the Flexport OTI for China to the U.S. West Coast and China to North Europe demonstrated a small downtick, while China to the U.S. East Coast plateaued.

Week to May 19, 2025

The Ocean Timeliness Indicator (OTI) The Ocean Timeliness Indicator (OTI) showed minor fluctuations again this week, with China to the U.S. West Coast decreasing from 36 to 35 days, and China to North Europe decreasing from 60.5 to 58.5 days. Meanwhile, China to the U.S. East Coast plateaued at 52.5 days.

About the Author

Related content

更多

![WarehouseGettyImages-535667233]()

Global Logistics Update

U.S. and Taiwan Finalize Trade Deal; FEWB Spot Rates Soften Amid Lunar New Year Lull

![Ocean Port GettyImages-1083936322 (1)]()

Global Logistics Update

EU to Vote on Modified U.S. Trade Deal; Ex-Asia Demand Tapers Off Ahead of Lunar New Year

![Air GettyImages-1343405900]()

Global Logistics Update

U.S. to Cut Tariffs on India; TPEB and FEWB Carriers Plan Upcoming Blank Sailings